If you’ve ever applied for a mortgage, car loan, or credit card, you probably heard the term “debt-to-income ratio” or DTI. It’s a simple number that shows lenders how much of your monthly income goes toward debt payments. A lower DTI means you have more breathing room, which makes lenders feel safer lending you money.

First, add up all your recurring monthly debt payments. Include mortgage or rent, car loans, student loans, credit‑card minimums, and any personal loans. Next, find your gross monthly income – that’s your paycheck before tax, plus any regular bonuses or side‑gig earnings.

Use this formula:

DTI = (Total Monthly Debt ÷ Gross Monthly Income) × 100%

For example, if you pay £1,200 in total debt each month and earn £4,000 before tax, your DTI is (1,200 ÷ 4,000) × 100 = 30%. Most lenders look for a DTI under 36%, and some prefer under 30% for the best rates.

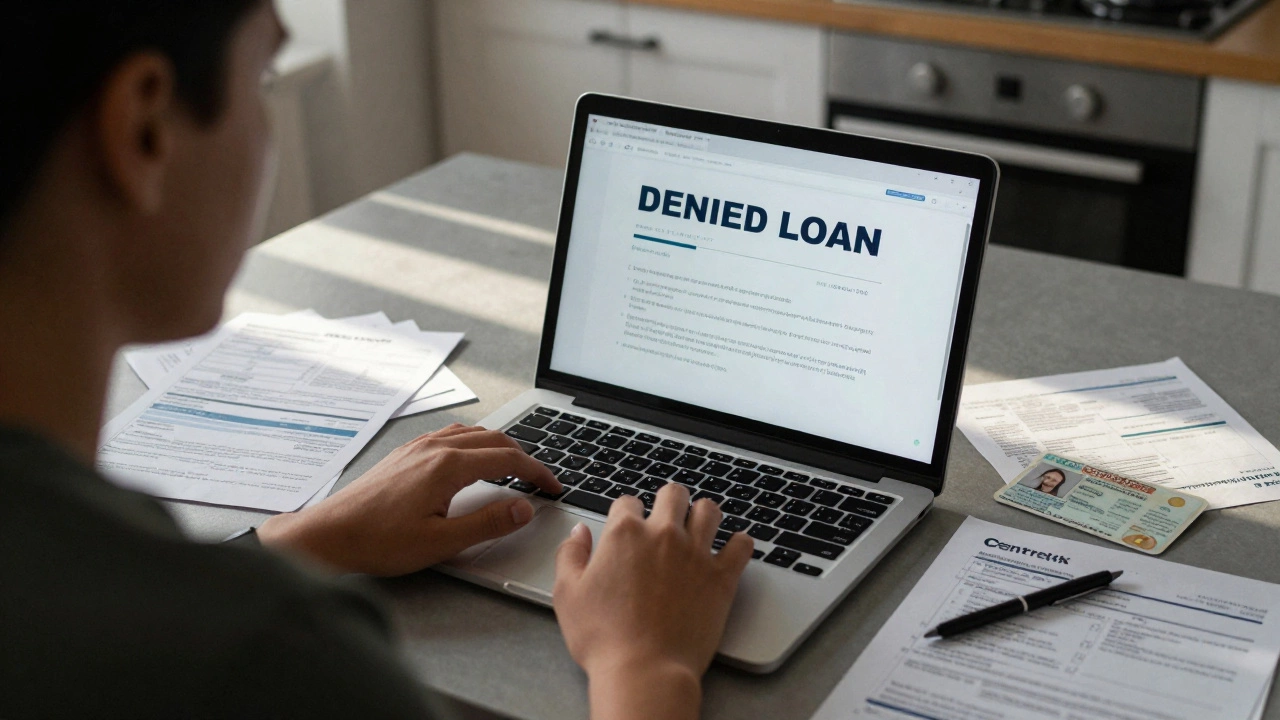

Lenders use DTI to gauge risk. A high DTI suggests you might struggle to make new payments if interest rates rise or if you lose a source of income. That risk often shows up as higher interest rates or a loan denial.

Besides loan decisions, a good DTI can help you qualify for better mortgage deals, lower car‑loan rates, and even affect the credit cards you’re offered. In short, keeping your DTI low opens doors to cheaper credit.

Now that you know what DTI is and how it’s calculated, let’s look at practical ways to improve it.

1. Pay down high‑interest debt first. Target credit‑card balances or payday loans. Reducing these balances shrinks your monthly payment quickly.

2. Re‑finance existing loans. If you can snag a lower rate on a mortgage or student loan, your monthly payment drops, which improves DTI.

3. Increase your income. A side gig, freelance work, or a raise all raise the denominator in the DTI equation, making the ratio better.

4. Avoid taking on new debt before applying. Hold off on opening new credit cards or financing a big purchase until after you get approved.

5. Consolidate debt. A personal loan with a lower rate can replace several higher‑rate loans, simplifying payments and often reducing the total monthly amount.

Remember, each small change adds up. Even a £100 reduction in monthly debt or a £200 boost in income can shave a few points off your DTI.

Finally, keep an eye on your credit report. Errors can inflate your apparent debt, hurting your DTI and credit score. Dispute any mistakes promptly.

Understanding and managing your debt-to-income ratio gives you more control over your financial future. Use the simple formula, track your numbers monthly, and apply the tips above to keep your DTI in a healthy range. When it’s low, lenders will see you as a low‑risk borrower, and you’ll enjoy better loan terms and more financial flexibility.

Many Australians are denied personal loans for reasons they don’t expect - not just bad credit. Learn the real reasons lenders say no, from unstable income to too much existing debt, and what you can do to fix it.

Find out if $100,000 of student debt is truly massive, how it compares to averages, its impact on life goals, and smart ways to manage or forgive it.

Wondering if you can qualify for debt consolidation? This article breaks down the key requirements, from your credit score and debt-to-income ratio to the types of debt you have. You'll find out which financial habits boost your chances, what lenders really look for, and pitfalls to dodge on your application. If you're thinking about rolling multiple payments into one, this guide cuts through confusion and helps you figure out your options. Discover tips to strengthen your odds and make the process smoother.