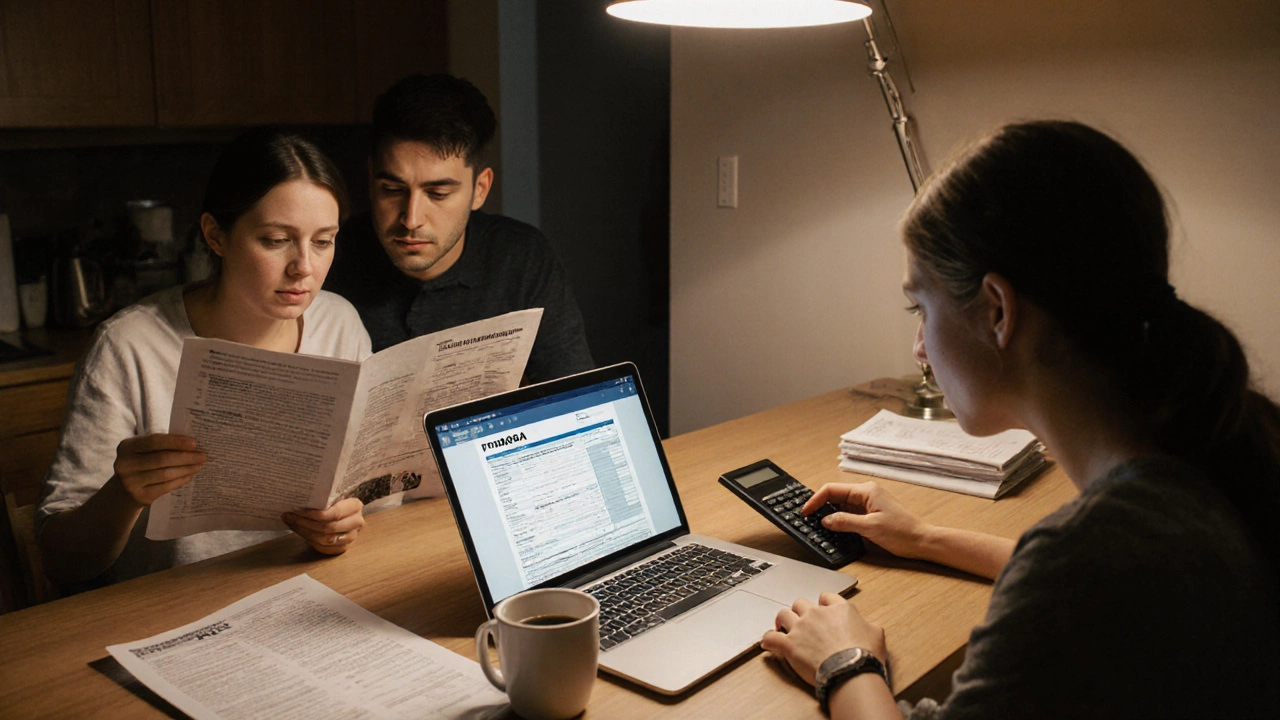

When thinking about finance, the management of money, including earning, spending, saving, investing, and protecting assets. Also known as personal or household finance, it’s what keeps your bills paid, your future secure, and your choices open. In October 2025, the big conversations revolve around when to act—and when to wait. Whether you’re watching crypto markets drop, weighing equity release options, or trying to stick to a budget, the real question isn’t just what’s happening—it’s what you should do about it.

equity release, a way for homeowners aged 55+ to unlock cash from their property without selling or moving. Also known as lifetime mortgages, it’s become a go-to tool for retirees in the UK who need extra income but want to stay in their homes. Interest rates in 2025 are still high, but smarter borrowers are comparing providers, reading the fine print on compound interest, and asking if they really need to tap into their home’s value. Meanwhile, crypto investing, buying and holding digital currencies like Bitcoin and Ethereum with the goal of profit. Also known as digital asset trading, it’s still wild, but October keeps proving it’s the worst month of the year—historically, prices drop 7% or more. Why? Tax season pressure, Fed policy shifts, and investor panic all line up. The smart move isn’t to bail out—it’s to understand the pattern and plan around it. And if you’re trying to keep your money on track, the 50/30/20 rule, a simple budgeting method that splits income into needs, wants, and savings. Also known as basic personal finance allocation, it’s one of the easiest ways to stop guessing and start growing your financial cushion. Home insurance? It didn’t drop in 2024—it went up 8.7%. If you’re still paying the same rate as last year, you’re likely overpaying. Switching isn’t hard, but you need to know what to look for: deductibles, coverage gaps, and hidden fees.

What you’ll find below isn’t theory. It’s real advice from people who’ve been there—whether they’re Australian retirees deciding on equity release, UK homeowners comparing insurance deals, or young earners trying to save $600 a month without burning out. No fluff. No jargon. Just clear, practical steps you can use right away. These posts answer the questions you didn’t even know to ask.

October is historically the worst month for crypto investing, with Bitcoin and Ethereum averaging 7%+ losses. Learn why seasonality matters, how tax cycles and Fed policy drive drops, and what to do instead of panicking.

Earning $70,000 doesn’t disqualify you from FAFSA aid. Learn how income, assets, and family size affect your eligibility for grants, loans, and work-study - and why filing is always worth it.

Home insurance rates didn't drop in 2024 - they rose by 8.7% on average. Learn why premiums increased, which areas were hit hardest, and what you can do to lower your costs now.

Find out where to get the best equity release in Australia in 2025. Learn how to choose a safe provider, avoid scams, and protect your pension and inheritance.

Learn what a toxic loan is, how it differs from regular loans, warning signs, and steps to avoid or escape one.

Learn how Australian savers can combine high‑yield accounts, term deposits, credit unions, P2P lending and low‑cost funds to target a 10% annual return while keeping risk low.

Learn the current equity release interest rates in 2025, how they're set, and steps to secure the best deal for UK and Australian homeowners.

Learn what defines upper class income, see international thresholds, and discover how it affects your investment strategy in clear, actionable steps.

Discover the #1 credit card for Australians in 2025, its rewards, fees, and how it compares to top alternatives.

Find out the lowest credit score Toyota will finance in Australia, how the score affects rates, and practical steps to secure a Toyota loan even with a marginal credit rating.

Discover whether equity release must be repaid, how lifetime mortgages work, key repayment triggers, and what to consider before unlocking home equity.

Learn which life insurance policies lock in premiums for life or a set term, compare whole, term, guaranteed issue, and fixed‑premium universal options.