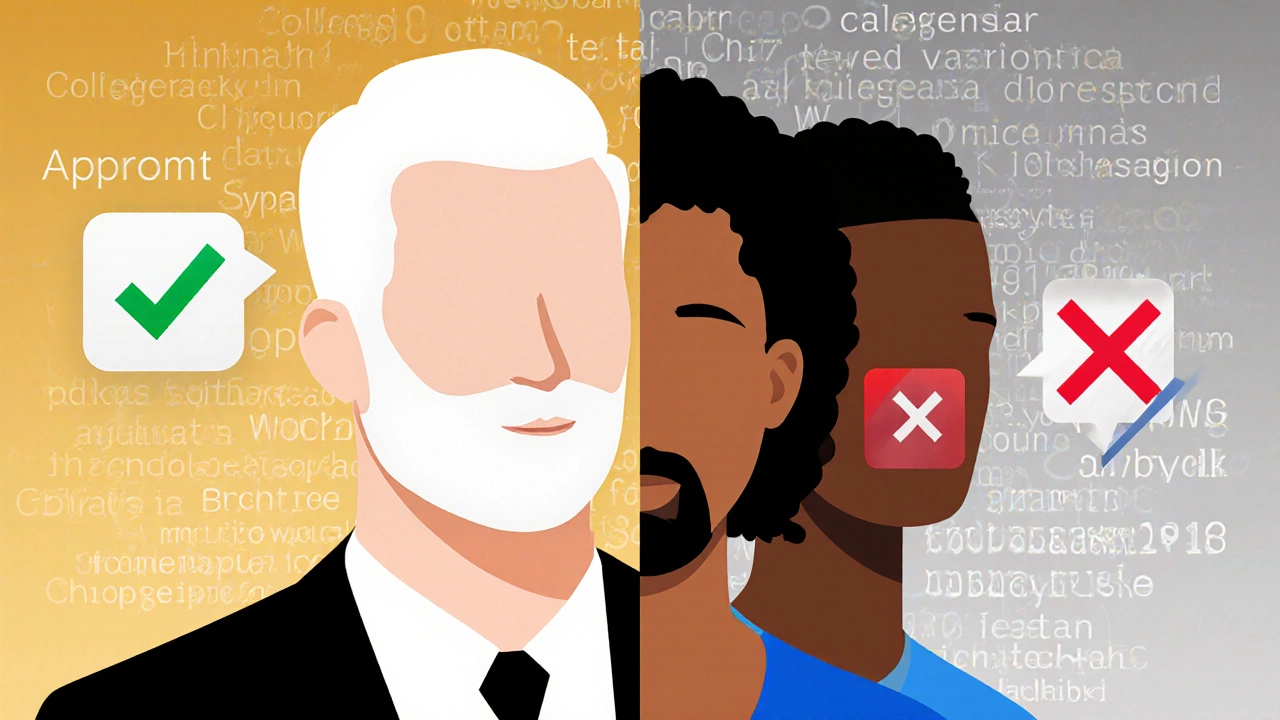

When you hear Upstart AI loans, a type of personal loan approved using artificial intelligence to assess creditworthiness instead of traditional credit scores. Also known as AI-powered lending, it’s marketed as faster, fairer, and more inclusive. But beneath the tech buzz, these loans carry the same risks as any high-interest debt—especially if you’re under pressure to borrow. Upstart doesn’t just look at your FICO score. It scans your education, job history, even your college major to decide if you qualify. That sounds great—if you’re a recent grad with a degree in engineering and no credit history. But if you’re self-taught, switched careers, or took time off to care for family? The algorithm might not see you as ‘low risk,’ even if you pay bills on time.

These loans often come with toxic loan, a loan with hidden fees, steep penalties, or terms that trap borrowers in long-term debt patterns. Interest rates can jump above 35% for people with thin files, and there’s no guarantee the rate you see upfront is the one you’ll get. Some users report being approved for $10,000 but only getting $5,000 after fees. And if you miss a payment? Late fees pile up fast, and your credit can tank—even if you were just one day late. This isn’t unique to Upstart. It’s the same pattern you see in payday loans, buy-now-pay-later traps, and predatory lending, lending practices that exploit vulnerable borrowers with unfair terms, high costs, or deceptive marketing across the industry.

What’s missing from the ads? Real alternatives. If you need money fast, a credit union personal loan might cost less. If you’re building credit, a secured card works better than an AI loan. And if you’re worried about your income not fitting a tech model? Talk to a local accountant. They’ve seen people get stuck in these loops—especially in places like Worcestershire, where paychecks are tight and emergencies are common. You don’t need an algorithm to tell you what you can afford. You just need honest numbers and a clear plan.

Below, you’ll find real stories and breakdowns of how these loans actually play out—what they cost, who gets hurt, and what to do instead. No hype. Just facts from people who’ve been there.

Upstart is being sued by the CFPB for using AI that discriminates against Black and Hispanic borrowers. Learn how its lending algorithm works, why it’s biased, and what this means for you if you’re applying for a personal loan.