Upstart Loan Approval Calculator

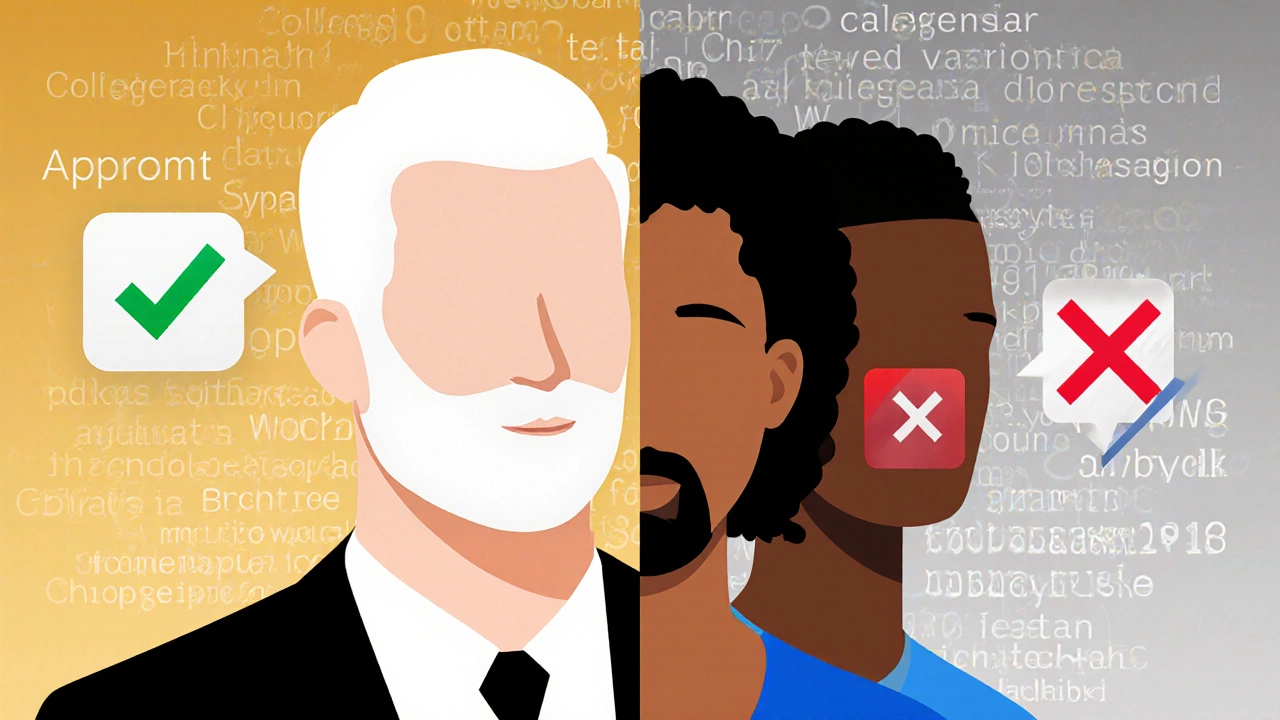

Based on the CFPB's findings, Upstart's AI model was 60% more likely to deny loans to Black applicants and 40% more likely to deny loans to Hispanic applicants compared to white applicants with identical financial profiles.

Your Application Profile

Note: This calculator is based on CFPB data from May 2024 showing racial disparities in Upstart's lending model. This simulation uses the reported statistics to show potential disparities, but individual loan outcomes depend on many factors. The CFPB found that for Black applicants with identical financial profiles to white applicants, the denial rate was 60% higher. For Hispanic applicants, it was 40% higher.

Upstart, once hailed as a tech-driven revolution in personal lending, is now at the center of a major legal storm. The company, which uses artificial intelligence to approve loans, is being sued by the Consumer Financial Protection Bureau (CFPB) for discriminatory lending practices. This isn’t just a regulatory hiccup-it’s a fundamental challenge to how AI is being used in finance. If you’ve ever applied for a personal loan through Upstart, or are considering it, you need to know what’s really going on.

What Upstart actually does

Upstart launched in 2012 with a simple pitch: use machine learning to judge your creditworthiness better than traditional banks. Instead of just looking at your credit score, they analyzed hundreds of data points-your education, job history, even your college major. The idea was to give people with thin credit files a fair shot. For a while, it worked. Upstart approved more loans to young borrowers and people of color than traditional lenders, and claimed lower default rates.

By 2023, Upstart had originated over $12 billion in loans. It partnered with banks to fund the loans, while Upstart handled the underwriting. The model looked smart. But behind the scenes, regulators started asking harder questions.

The CFPB lawsuit: what they’re accusing Upstart of

In May 2024, the CFPB filed a federal lawsuit against Upstart, alleging violations of the Equal Credit Opportunity Act (ECOA). The core claim? Upstart’s AI model disproportionately denies loans to Black and Hispanic applicants-even when they have the same income, credit history, and debt levels as white applicants.

The CFPB’s analysis found that Upstart’s algorithm was 60% more likely to deny a loan to a Black applicant than a white applicant with identical financial profiles. For Hispanic applicants, the denial rate was 40% higher. These aren’t small differences. These are systemic.

Upstart claims its model doesn’t use race, gender, or zip code as inputs. That’s true. But the CFPB argues the algorithm still picks up proxies for race. For example, the model heavily weights the name of your college. Schools with higher proportions of Black or Hispanic students-like historically Black colleges-were penalized in the scoring. The same thing happened with job titles common in minority communities. Even the way someone spells their name (e.g., "DeShawn" vs. "Deshawn") affected approval odds.

Why AI can still be biased

This isn’t a glitch. It’s a known problem in machine learning. AI doesn’t think. It finds patterns in data. And if the data reflects past discrimination, the AI learns to replicate it.

Upstart’s training data included millions of loans approved or denied by traditional banks over the past 20 years. Those banks had long histories of redlining, underwriting bias, and unequal access to credit. The AI didn’t invent bias-it just learned it better and faster.

Think of it like this: if you train a model on decades of hiring data where men were promoted more often than women, the AI will learn to favor men-even if you tell it not to use gender. The same thing happened with Upstart. The algorithm didn’t need race to be a variable. It found race in the details.

What Upstart says in its defense

Upstart denies any intentional discrimination. Their public statements say they’re committed to fair lending and that their model helps underserved borrowers. They point to their own internal audits, which showed higher approval rates for minority applicants compared to traditional lenders.

But the CFPB’s lawsuit includes internal emails and model documentation that contradict this. One 2021 memo from Upstart’s head of risk management warned: "Our model’s performance on Black applicants is significantly worse than on white applicants. We need to fix this before regulators notice."

Upstart also argues that their model is more accurate than traditional credit scoring. That may be true. But accuracy doesn’t equal fairness. A model can predict defaults well and still deny loans unfairly. You can be precise and still be unjust.

What this means for borrowers

If you’re thinking of applying for an Upstart loan, here’s what you should know:

- Approval odds might still be better than traditional lenders-if you’re white, middle-class, and went to a top-tier university.

- If you’re a person of color, especially with a non-traditional education or job path, you could be silently penalized.

- Upstart doesn’t tell you why you were denied. Unlike banks, they don’t give you a reason code. That makes it impossible to fix your application.

- There’s no appeal process. If the AI says no, that’s final.

And here’s the kicker: Upstart still markets itself as "fairer" and "more inclusive." Their ads show diverse families buying homes and paying off debt. But the data tells a different story.

What’s next for Upstart

The lawsuit is still in early stages. Upstart could settle, change its model, or fight it in court. But the CFPB isn’t alone. The Department of Justice is also reviewing the case. At least two class-action lawsuits have been filed by borrowers.

Some banks that partnered with Upstart have already paused new lending deals. Ally Financial and Cross River Bank-two major funding partners-stopped originating new Upstart loans in late 2024. That’s a huge red flag. Banks don’t walk away from profitable partnerships unless they see serious legal risk.

If Upstart loses, it could face fines in the hundreds of millions. It might be forced to stop using its current AI model. Or worse-it could be banned from using certain data inputs altogether. That would mean going back to the drawing board.

What you can do

Don’t assume AI is fair just because it’s new. Don’t assume a tech company has your best interests at heart. Here’s how to protect yourself:

- Check your credit report. Make sure there are no errors that could hurt your score.

- Apply to multiple lenders. Compare offers from banks, credit unions, and online lenders-not just Upstart.

- If you’re denied, ask for a reason. Even if Upstart doesn’t give you one, other lenders will.

- Report suspected discrimination. File a complaint with the CFPB at consumerfinance.gov/complaint.

Upstart’s story isn’t just about one company. It’s about a larger trend: the rush to automate finance without asking who gets left behind. AI isn’t neutral. It reflects the world it was trained on-and that world still has deep, ugly biases.

If you’re looking for a personal loan, don’t just pick the one with the lowest rate. Ask: who designed this? Who benefits? And who’s being left out?

Is Upstart still giving out loans?

Yes, Upstart is still originating loans as of November 2025. But several of its bank partners have paused new deals. Loans are still being funded, but the volume has dropped significantly. If you apply now, your chances of approval may be lower than in previous years.

Can I sue Upstart if I was denied a loan?

You may be eligible to join a class-action lawsuit if you’re a Black, Hispanic, or other minority borrower who was denied a loan between 2018 and 2024. Legal teams are actively gathering applicants. You don’t need to pay anything upfront-most cases are handled on a contingency basis. Check with a consumer rights attorney or visit the CFPB’s website for updates on active litigation.

Why doesn’t Upstart disclose why it denies loans?

Upstart claims its AI model is too complex to explain in simple terms. But the CFPB argues this is a tactic to avoid accountability. Federal law requires lenders to provide specific reasons for denial. Upstart’s refusal to do so may itself be a violation of the law. Other lenders-even those using AI-give reason codes. Upstart does not.

Are there safer AI-powered lenders than Upstart?

Some lenders, like Avant and SoFi, use AI too-but they’ve been more transparent about their models and have faced fewer discrimination claims. Credit unions using AI, like Alliant Credit Union, also tend to have stronger fairness audits. Always look for lenders that provide clear denial reasons and publish annual fairness reports.

What happens if Upstart goes out of business?

Your loan doesn’t disappear. Upstart doesn’t fund the loans-it partners with banks. So even if Upstart shuts down, your loan is still owned and managed by the bank that funded it. You’ll still need to make payments. The only difference? You’ll deal with the bank directly, not Upstart’s platform.