When you hear upstart lending practices, new, tech-driven loan models that bypass traditional banks using algorithms and alternative data. Also known as digital lending, it’s meant to make borrowing faster and easier—especially for people with thin credit files. But speed doesn’t always mean safety. These lenders use your phone usage, social media activity, or even your grocery habits to decide if you qualify. Sounds futuristic? It is. But it’s also turning into a minefield for people who don’t fully understand what they’re signing up for.

One big problem? Many of these loans come with toxic loans, credit products designed to trap borrowers in cycles of debt through hidden fees, short terms, and sky-high interest. Also known as predatory lending, these aren’t illegal—but they’re engineered to exploit financial desperation. Think $500 loans with $100 fees and 400% APR, rolled into monthly payments you can’t afford. That’s not finance—it’s a trap. And it’s not rare. In fact, several of the posts below show how people end up deeper in debt after chasing quick cash through these new platforms.

What makes this worse is that high-interest loans, loans with APRs far above the national average, often targeting low-income or credit-challenged borrowers are being marketed as "affordable" or "inclusive." But if your payment doubles in six months, or your balance grows because you can’t make the minimum, that’s not inclusion—it’s exploitation. And it’s happening more than you think.

You’ll find real stories here: people who took out a $2,000 loan to fix their car, only to pay back $8,000 over two years. Others who thought a 0% APR credit card was a gift, until the promo ended and their balance exploded. These aren’t outliers. They’re symptoms of a system built to profit from financial stress.

This collection doesn’t just list problems. It shows you how to recognize the red flags before you sign. You’ll see how income thresholds, credit scores, and even your zip code can influence whether you’re offered a fair deal—or a rigged one. Whether you’re considering a personal loan, a balance transfer, or an equity release, the same rules apply: if it sounds too good to be true, it probably is. And if the fine print is buried under five layers of app screens, walk away.

Below, you’ll find clear, no-fluff breakdowns of the loans people are falling for—and how to avoid them. No jargon. No hype. Just facts from real cases. Because when it comes to your money, you deserve more than a quick fix. You deserve to understand what you’re getting into.

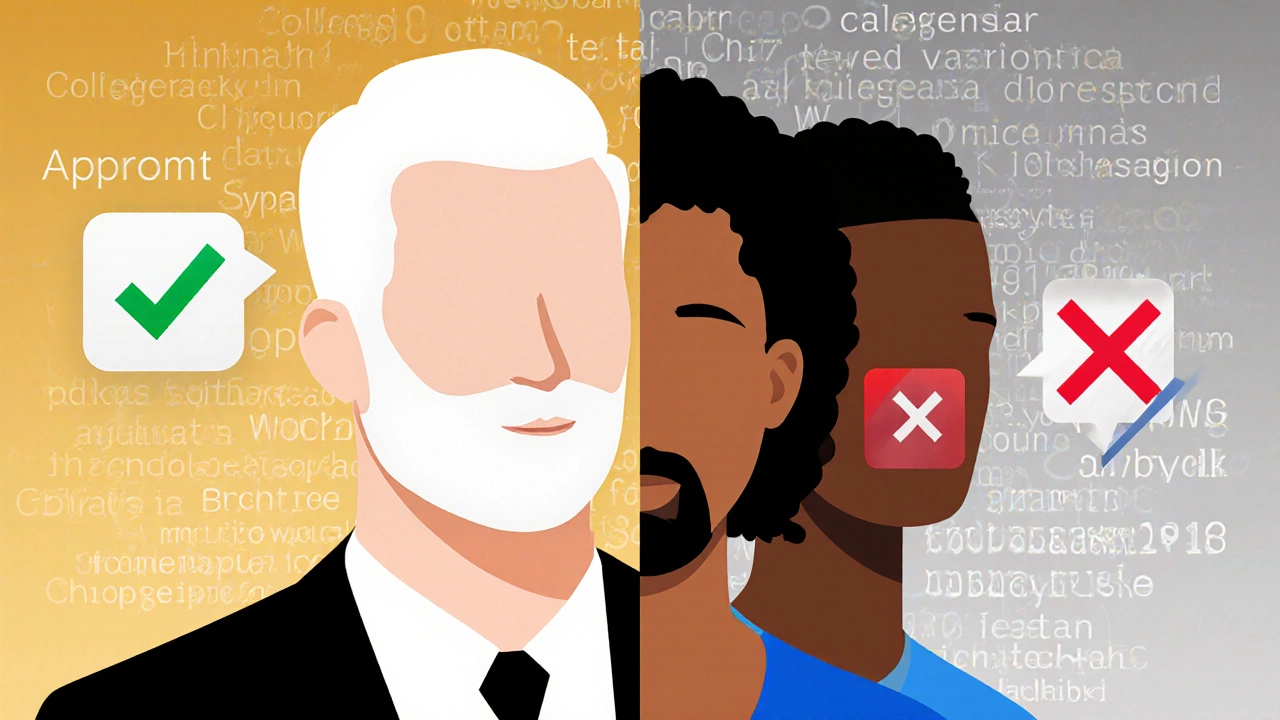

Upstart is being sued by the CFPB for using AI that discriminates against Black and Hispanic borrowers. Learn how its lending algorithm works, why it’s biased, and what this means for you if you’re applying for a personal loan.