When you need cash fast and your credit history isn’t perfect, Upstart personal loans, an online lending platform that uses AI to assess creditworthiness beyond traditional scores. Also known as AI-powered personal loans, it’s become a go-to for people turned down by banks but still need money for debt consolidation, medical bills, or car repairs. Unlike traditional lenders that only look at your FICO score, Upstart considers education, job history, and field of work—giving more people a shot at approval. But this doesn’t mean it’s easy money. The same tech that helps you get approved can also lock you into higher rates if you’re not careful.

Many people don’t realize that Upstart, a fintech lender founded in 2012 and backed by investors like Google. Also known as AI-driven lender, it doesn’t actually lend the money itself—it connects borrowers with third-party banks. That means terms can vary wildly depending on which bank is funding your loan. Some users get rates as low as 5.99%, while others end up paying over 35%—especially if they have a short credit history or no income verification. This isn’t a scam, but it’s not a safety net either. It’s a tool. And like any tool, it can help you or hurt you depending on how you use it.

Another thing most people miss: origination fees, a one-time charge lenders apply when you take out a loan, often between 0% and 8%. Also known as loan processing fee, it can eat into your cash upfront. If you borrow $10,000 with a 5% fee, you only get $9,500—but you still pay interest on the full $10,000. That’s a hidden cost that makes the APR misleading. And while Upstart doesn’t charge prepayment penalties, some of its lender partners might. Always read the fine print—even if the website looks clean and simple.

What makes Upstart different from payday lenders? It doesn’t trap you in a cycle of rollovers. You get a fixed term—usually 3 or 5 years—with consistent payments. But that also means you’re locked in. If your income drops, you still owe the same amount. And if you miss a payment, your credit score takes another hit, making it harder to refinance later. This isn’t a quick fix—it’s a long-term commitment dressed up as a quick solution.

So who actually benefits? People with steady jobs, college degrees, or in-demand skills—even if their credit score is below 600. If you’ve been turned down by a bank and have a clear plan for how to use the money, Upstart can be a real lifeline. But if you’re using it to cover everyday expenses or pay off other high-interest debt without changing your spending habits, you’re just moving the problem around.

Below, you’ll find real stories and breakdowns from people who’ve used Upstart—some saved money, others got stuck. We’ll show you how to compare offers, what documents to have ready, and how to spot the red flags before you click "Apply." This isn’t about pushing loans. It’s about helping you make smart choices when the system isn’t designed to help you.

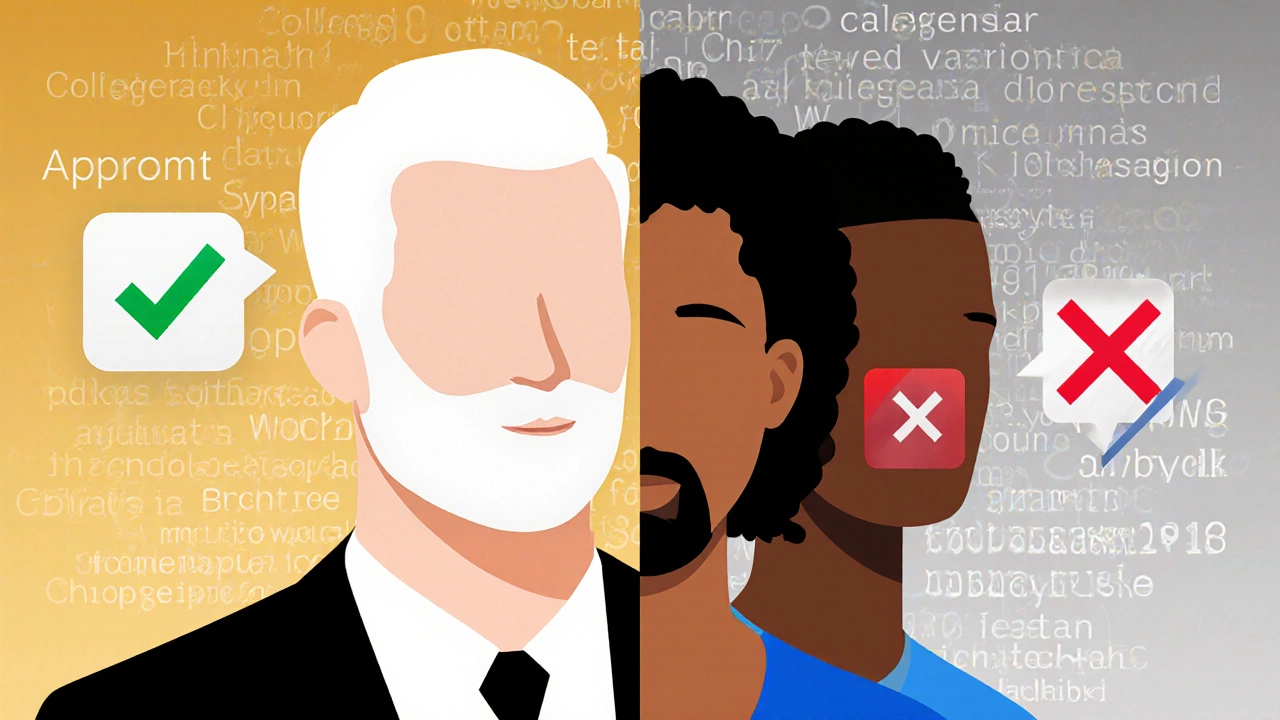

Upstart is being sued by the CFPB for using AI that discriminates against Black and Hispanic borrowers. Learn how its lending algorithm works, why it’s biased, and what this means for you if you’re applying for a personal loan.