Got several loans, credit‑card balances, and a mounting bill that feels impossible to manage? You’re not alone. Many people in Worcestershire end up juggling multiple payments and high interest rates. Combining those debts into one payment can cut the stress and often lower the overall cost. Let’s walk through what debt consolidation is, when it makes sense, and how to pick the right option for you.

First off, consolidation means you take all your existing debts and replace them with a single loan or payment plan. The biggest perk is a single due date – no more hunting for different statements every month. If you can secure a lower interest rate, the total you pay over time drops, freeing up cash for other needs. It also simplifies budgeting; you know exactly how much you owe each month, which can improve your credit score over time.

There isn’t a one‑size‑fits‑all answer. A personal loan from a bank or building society is popular because it offers a fixed rate and repayment term. Credit unions in Worcestershire often have lower fees and more flexible criteria, especially if you’ve struggled with credit in the past. Balance‑transfer credit cards can work if you can pay off the balance before the promotional period ends. Finally, specialist debt‑consolidation firms may bundle all debts into one monthly payment, but you’ll need to watch for hidden fees.

Before you sign anything, do a quick debt inventory. List every loan, the amount owed, interest rate, and monthly payment. Add up the total you owe and compare it to the amount you’d need to borrow in a new loan. If the new monthly payment is lower and the interest rate is favorable, you’re on the right track.

Check your credit score next. A higher score gives you access to better rates. If your score is low, consider a short‑term fix like a smaller personal loan to improve it before applying for a larger consolidation loan.

Now, shop around. Use a spreadsheet or an online calculator to compare interest rates, repayment terms, and any setup fees. Remember that a longer term reduces your monthly payment but can increase the total interest paid. Find a balance that matches your cash flow and long‑term goals.

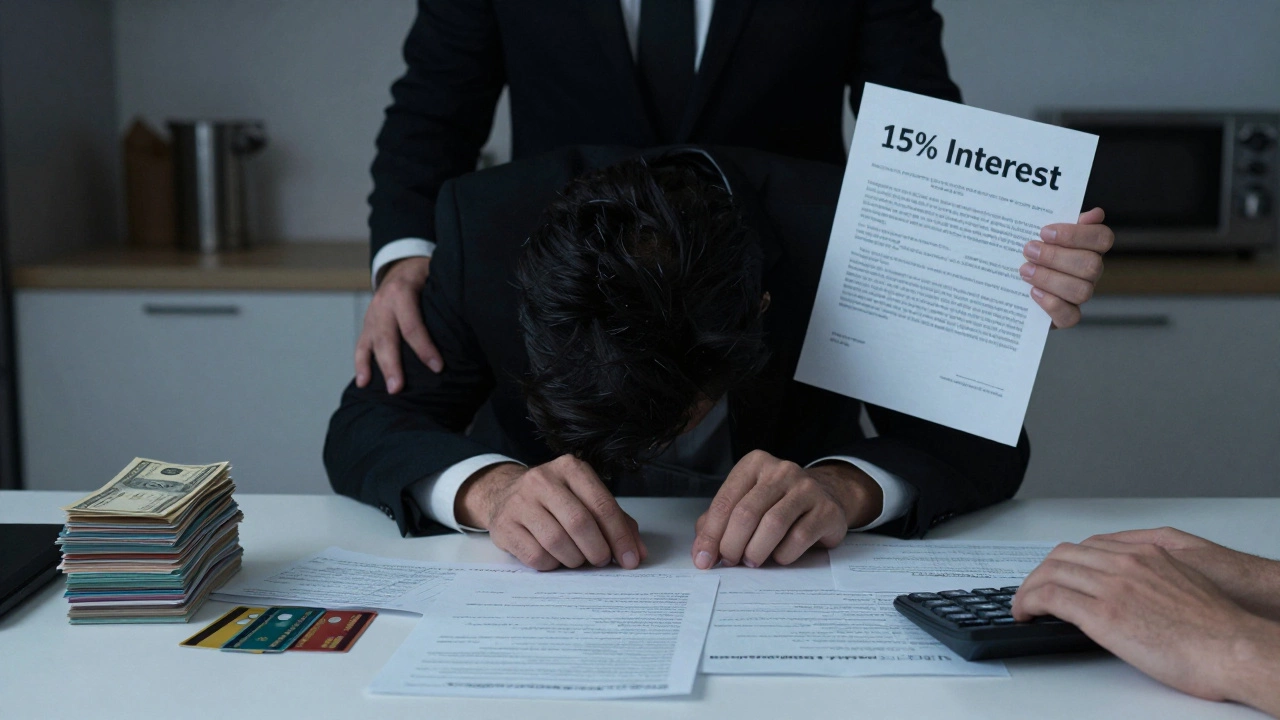

When you’ve narrowed down a few options, read the fine print. Look for early repayment penalties, arrangement fees, or variable‑rate clauses that could change your payment later. Ask the lender how they handle missed payments – some offer temporary relief, while others may charge hefty fees.

Once you’ve selected a plan, gather the required documents: proof of identity, address, income, and details of your existing debts. Most lenders will run a quick credit check and then give you a decision within a few days.

After the consolidation loan is approved, the lender will usually pay off your existing creditors directly. Double‑check that each old account shows a zero balance. Keep an eye on the first few statements to ensure everything is recorded correctly.

If you’re unsure which route fits your situation, the team at Worcestershire Finance Experts can help. Our accountants can run the numbers, spot hidden costs, and recommend the most suitable product for your financial picture.

Finally, stick to the new payment plan. Avoid taking on fresh debt while you’re paying off the consolidated loan – that defeats the purpose. Set up a direct debit to avoid missed payments, and watch your credit score improve as you make regular, on‑time payments.

Debt consolidation isn’t a magic fix, but it can be a powerful tool to regain control of your finances. With a clear plan, the right lender, and a bit of discipline, you’ll move from juggling multiple bills to a single, manageable payment. Ready to start? Grab a pen, list your debts, and take the first step toward a cleaner financial future.

Discover how debt relief impacts your credit score. Learn the differences between settlement, consolidation, and bankruptcy, and find out how to rebuild your credit fast.

Discover if debt consolidation hurts your credit score. Learn about hard inquiries, credit utilization, and strategies to protect your rating while paying off debt faster.

Find out if debt consolidation cancels your credit cards. Learn the differences between personal loans, balance transfers, and DMPs, and how each affects your credit score and card status.

Debt consolidation can temporarily lower your credit score due to hard inquiries and changes in credit utilization-but when managed well, it helps rebuild credit over time by simplifying payments and encouraging on-time behavior.

Debt consolidation seems simple but often fails due to high interest rates, strict lending rules, and unchanged spending habits. Learn why it's hard to qualify, what really works, and how to break the cycle without falling for scams.

Discover the credit score requirements for debt consolidation loans. Learn how lenders evaluate your score, options for lower scores, and steps to improve your chances. Get clear facts to make informed decisions about managing debt.

National debt relief isn't a government program-it's a marketing term used by private companies. Learn how debt settlement really works, why it often backfires, and what actually helps people get out of debt without wrecking their credit.

Worried about being denied debt consolidation? Discover the real reasons, how it works, and practical steps if you get rejected for a consolidation loan.

Wondering if unpaid debt just vanishes after seven years? This article breaks down what really happens after you ignore a debt for that long. You'll find out how your credit report changes, whether collectors can still chase you, and what 'statute of limitations' means for your bank account. Plus, get smart tips on handling old debts and avoiding common mistakes. Cut through the myths and learn what to really expect after seven years without making payments.

Wondering if you can qualify for debt consolidation? This article breaks down the key requirements, from your credit score and debt-to-income ratio to the types of debt you have. You'll find out which financial habits boost your chances, what lenders really look for, and pitfalls to dodge on your application. If you're thinking about rolling multiple payments into one, this guide cuts through confusion and helps you figure out your options. Discover tips to strengthen your odds and make the process smoother.

Debt consolidation sounds easy, but it can backfire if you're not careful. This article dives into the drawbacks and hidden risks you might face when rolling your loans into one. You'll learn why lower payments aren't always a win and how your credit could take a hit. Find out about tempting traps, added costs, and why this move doesn't actually erase debt. Real tips and honest talk—no sugarcoating.

Struggling to get a loan approval can be frustrating, especially when bills pile up. Explore alternative strategies like debt consolidation to manage existing debts without traditional loans. Learn how to improve your credit score and explore unconventional loan sources. We provide insights into dealing with loan refusals by enhancing financial credibility. This guide offers practical advice for charting a path towards financial stability.