Did you know most people lose around £1,000 a year by ignoring simple money habits? The good news is you can stop the leak with a few practical steps. Below you’ll find short, down‑to‑earth advice that works whether you’re saving for a house, paying down debt, or just trying to stretch your paycheck a bit further.

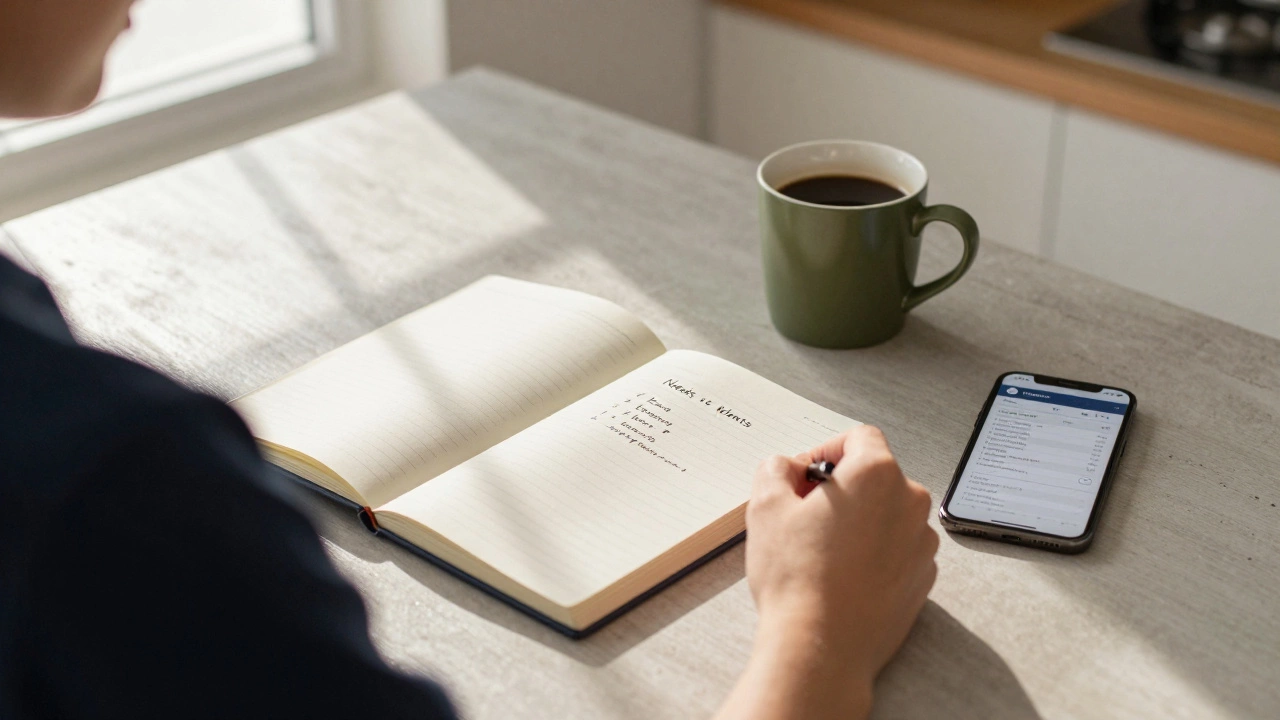

First things first – know where every pound goes. Grab a spreadsheet, a notebook, or a budgeting app and write down three categories: must‑pay (rent, bills, loan repayments), needs (groceries, transport) and wants (eating out, streaming). Give each a realistic amount and stick to it for a month. If you find you’re consistently overspending on wants, trim a little. Even a £10 cut every week adds up to over £500 in a year.

One simple trick is the “20/30/50” rule: aim to allocate 20% of your net income to savings and debt repayment, 30% to flexible spending, and 50% to essential costs. It’s not a hard law, but it gives you a clear target. Adjust the percentages to fit your circumstances – if you have high mortgage payments, shift a bit more into the essential bucket and keep the savings goal steady.

Saving doesn’t have to mean locking away all your money. Start with a micro‑goal like putting £20 aside each week. Over 52 weeks you’ll have £1,040 before interest. Add a modest 1%‑2% savings account rate and you’ll see a few extra pounds in your balance – enough to motivate you to keep going.

If you’re a UK resident, check whether an ISA (Individual Savings Account) fits your plan. ISAs let you earn interest or investment returns tax‑free up to the annual limit. Even if you’re not a UK citizen, there are options for non‑residents to open a “non‑resident ISA” – it’s worth a quick chat with a local accountant.

Got equity in your home? You don’t have to sell, but you can explore pull‑out options like a HELOC or a cash‑out refinance if you need a lump sum for a renovation or debt consolidation. Just remember the loan‑to‑value (LTV) ratio – lenders usually want you to keep at least 20% equity untouched.

On the debt side, if a consolidation loan gets denied, look at the reasons: low credit score, high existing debt, or missing documentation. Fixing these – by paying a small bill on time or updating your income proof – can improve your chances next time.

Credit cards are another tool. When comparing cards, focus on the annual fee, interest rate, and rewards that match your spending habits. A card with a low fee and a decent cash‑back rate can save you money faster than a high‑reward card that charges 30% in fees.

Finally, think about the future. Pensions, 401(k)s, and other retirement plans may look complicated, but the basic idea is the same: contribute early, let compound interest work for you, and consider the tax implications. Even a modest monthly contribution can grow significantly over a 30‑year span.

All these tips fit into a single, manageable plan: set a realistic budget, automate a small weekly saving, keep an eye on debt‑repayment options, and use tax‑advantaged accounts where possible. You don’t need a finance degree to improve your money health – just a few minutes each week and the willingness to adjust.

Ready to get started? Pick one of the ideas above, take the first step today, and watch your financial confidence grow. Need personalized advice? Our team at Worcestershire Finance Experts is here to help you tailor a plan that works for your life.

Learn the 7 practical steps to build a real budget that works-no deprivation, no guesswork. Track spending, set goals, automate savings, and build a buffer for surprises. Take control of your money today.

The 50/30/20 rule splits your after-tax income into 50% needs, 30% wants, and 20% savings/debt. It's a simple, flexible way to budget without feeling restricted. Learn how to apply it to your life and start building real financial security.

The 30-40-30 rule is a flexible budgeting method that splits your take-home pay into 30% for needs, 40% for wants, and 30% for savings and debt. It works better than 50-30-20 in high-cost cities like Sydney and helps you save without feeling deprived.

Discover the simple Golden Rule Budgeting method, how it works, benefits, pitfalls, and a quick start checklist for effective money management.

The 50 30 20 rule of budgeting is a simple way to manage your money without drowning in spreadsheets. By splitting your income into needs, wants, and savings, you can keep your spending in check and hit your financial goals faster. This article explains what the 50 30 20 rule is, how it actually works, and how to fit it into real life—even when things aren’t perfect. We’ll dig into common mistakes, hacks for sticking to the plan, and how to tweak the rule when life gets off track. If you’re looking for a no-nonsense approach to budgeting, this is for you.

Figuring out whether to stash your cash in a savings or checking account can be tricky. Let's break down the differences, share some cool facts, and help you make the best choice for your financial goals. Learn about interest rates, account features, and pro tips for managing your money smartly.

The Golden Budget Rule is a simple yet powerful tool to help manage your finances more effectively. It divides your income into essential expenses, savings, and discretionary spending, providing a clear path to financial stability. This approach not only ensures you cover necessities but also encourages saving habits and allows for fun spending. Discover how to personalize it to fit your unique financial situation and learn tricks to maximize its benefits.

Discover the 70 15 15 budget, an effective way to manage your finances by allocating 70% of your income to needs, 15% to savings, and 15% to wants. This approach helps prioritize essential expenses while still allowing room for enjoyment and future planning. Learn how to implement this strategy, its benefits, and tips for making it work for your lifestyle.

Withdrawing money from a savings account may seem straightforward, but it carries potential downsides that could impact your financial well-being. This article explores the various drawbacks, such as potential withdrawal penalties, loss of interest, and their effect on long-term savings. We'll also take a look at alternatives to consider and tips on managing your savings more effectively. Dive in to learn about the implications of dipping into your savings and how to navigate these challenges.

Overcoming a $30,000 debt in just twelve months might seem daunting, yet it’s entirely possible with focused strategies. This guide explores practical methods, from creating a budget and increasing income to negotiating with creditors and consolidating loans. Whether you're drowning in credit card debt or struggling under student loans, these steps provide actionable insights. Embrace these tips and move towards a debt-free life with confidence.

Many people find themselves wondering if it's wise to keep large sums of money in a checking account. This article delves into the pros and cons of this financial strategy, exploring how it can impact one's financial goals. We'll discuss considerations when deciding how much money to maintain in your checking account and provide tips to optimize your savings. Whether focusing on accessibility, security, or growth potential, this guide will help you make informed decisions about your financial well-being.

This article dives into the 60 40 budget rule providing practical insights and tips for personal finance enthusiasts. It explains how dividing your income into essential needs and savings can help you manage your money wisely. Learn about this flexible approach and discover ways to tailor it to your individual financial situation. Whether you're new to budgeting or looking to refine your approach, this guide offers clarity and direction. Gain financial confidence through structured money management strategies.