30-40-30 Budget Calculator

How to use this calculator

Enter your monthly take-home pay to see how the 30-40-30 rule allocates your income. The rule divides your income into three parts: 30% for essential needs, 40% for discretionary spending, and 30% for savings and debt repayment.

Note: This is a flexible framework - adjust percentages based on your personal situation.

Ever feel like your paycheck disappears before the end of the month, even when you think you’re being careful? You’re not alone. Most people don’t struggle because they earn too little-they struggle because they don’t have a clear system for where their money goes. That’s where the 30-40-30 rule comes in. It’s a simple, no-fluff way to split your take-home pay so you actually save, spend wisely, and still enjoy life without guilt.

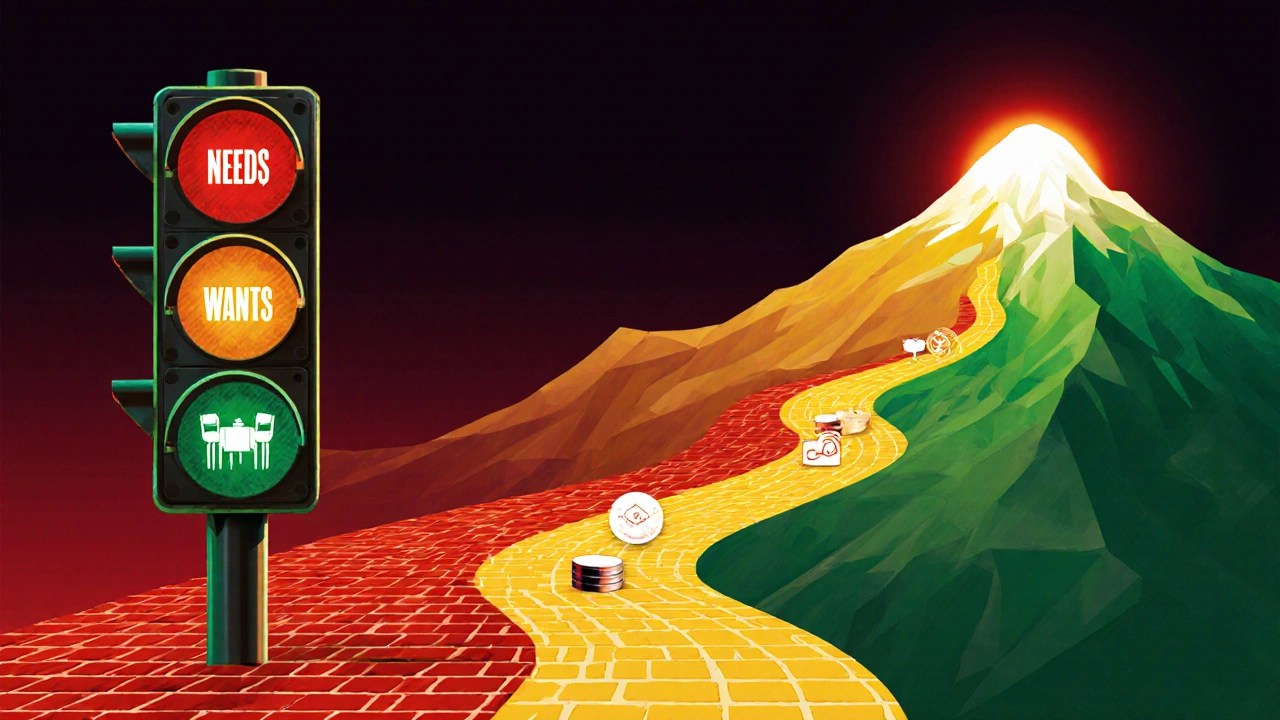

What exactly is the 30-40-30 rule?

The 30-40-30 rule is a budgeting method that divides your monthly take-home income into three buckets:

- 30% for needs-things you absolutely must pay to survive and stay functional.

- 40% for wants-everything that makes life enjoyable but isn’t essential.

- 30% for savings and debt repayment-building your future, paying off loans, or preparing for emergencies.

It’s not a rigid law. It’s a flexible framework designed for real life-not theoretical budgets that collapse the second you go out for coffee with friends.

Think of it like a traffic light: green for savings (go), yellow for wants (proceed with care), red for needs (non-negotiable). The rule forces you to make conscious choices instead of letting spending happen by accident.

How to apply the 30-40-30 rule step by step

Let’s say your take-home pay after taxes is $4,000 a month. Here’s how it breaks down:

- Calculate 30% for needs - $1,200. This covers rent or mortgage, utilities, groceries, basic transportation, minimum debt payments, essential insurance, and basic healthcare. If your rent is $1,500, you’ve already gone over. That’s okay-you adjust elsewhere. The goal isn’t perfection, it’s awareness.

- Calculate 40% for wants - $1,600. This is your freedom zone. Dining out, subscriptions, hobbies, clothes, travel, gifts, entertainment. If you spend $800 on Netflix, Spotify, Amazon Prime, and Apple Music, you’ve used half your wants budget already. That’s fine-just know it.

- Calculate 30% for savings and debt - $1,200. This is your future self’s lifeline. Put it into an emergency fund, retirement account, or extra payments on high-interest debt. If you have $5,000 in credit card debt at 22% interest, throwing $800 a month at it will wipe it out in under a year. That’s life-changing.

Track your spending for one month using a free app like PocketGuard or even a simple spreadsheet. At the end of the month, see where you actually landed. Did you spend 50% on wants? Did you skip savings entirely? That’s your starting point for adjustment.

Why the 30-40-30 rule works better than 50-30-20

You’ve probably heard of the 50-30-20 rule-50% needs, 30% wants, 20% savings. It’s popular, but it doesn’t match reality for most people in Australia today.

Housing costs in Sydney and Melbourne have skyrocketed. A single person renting a one-bedroom apartment might spend $2,200 a month on rent alone. That’s already 55% of a $4,000 income. Under 50-30-20, that person would be forced to either live in a garage or break their budget. The 30-40-30 rule flips the script: it assumes needs are already high, so it gives you more room for wants and still protects savings.

Here’s a quick comparison:

| Category | 30-40-30 Rule | 50-30-20 Rule |

|---|---|---|

| Needs | $1,200 (30%) | $2,000 (50%) |

| Wants | $1,600 (40%) | $1,200 (30%) |

| Savings & Debt | $1,200 (30%) | $800 (20%) |

See the difference? The 30-40-30 rule gives you $400 more for fun and $400 more for your future. That’s not a small win. It’s the difference between feeling trapped and feeling in control.

Who benefits most from the 30-40-30 rule?

This rule shines for people who:

- Live in high-cost cities (Sydney, Melbourne, Brisbane)

- Have student loans or credit card debt

- Work freelance or have irregular income

- Feel guilty about spending on themselves

- Want to save but don’t know where to start

It’s also great for young professionals who don’t have dependents yet but want to build wealth early. If you’re 28, earning $55,000 a year after tax, and you’re not saving anything, the 30-40-30 rule gives you a realistic path to $10,000 saved in a year-not by cutting out coffee, but by shifting how you think about money.

Pitfalls to avoid

The 30-40-30 rule isn’t magic. It fails if you misclassify expenses.

Mistake #1: Calling everything a need. That $120 monthly gym membership? If you haven’t used it in six months, it’s a want. Your Netflix subscription? Want. Your phone bill? Need. But if you’re paying $150 for premium data and streaming packages you barely use? That’s a want too.

Mistake #2: Ignoring irregular expenses. Car registration, annual insurance, holiday gifts-these don’t show up every month. Plan for them. Divide your yearly costs by 12 and add them to your needs or savings bucket. For example, if car registration is $600 a year, add $50/month to savings.

Mistake #3: Forgetting to adjust. Your income changes? You got a raise? You lost a job? Your budget must change too. Revisit the 30-40-30 split every three months. If your rent goes up by $300, you might need to trim wants by $200 and savings by $100. That’s not failure-it’s adaptation.

Real-life example: Sarah’s story

Sarah, 31, works in marketing in Sydney. Her take-home pay is $4,200 a month. Before the 30-40-30 rule:

- Rent: $2,100

- Utilities, phone, internet: $400

- Food: $500

- Subscriptions: $150

- Dining out: $400

- Shopping: $300

- Savings: $0

- Credit card debt: $8,000

She was stressed, broke, and always behind. She applied the 30-40-30 rule:

- Needs (30% = $1,260): Rent ($2,100) was too high. She moved to a smaller place with a flatmate, bringing rent down to $1,100. Utilities and groceries now total $450. Total needs: $1,550. She paid the extra $290 toward her credit card.

- Wants (40% = $1,680): She kept her $150 subscriptions and $300 shopping budget. She cut dining out from $400 to $200. She added $150 for weekend trips. Total wants: $1,550. She had $130 left over to save.

- Savings & Debt (30% = $1,260): She put $1,000 toward her credit card and $260 into a high-interest savings account. She paid off her credit card in 8 months.

Now, Sarah has $7,000 saved, no credit card debt, and still goes out for dinner twice a month. She didn’t become a monk. She just got smarter.

What if you can’t stick to the numbers?

You don’t need to hit 30-40-30 perfectly on day one. Start where you are.

If you’re only saving 5% right now, aim for 10%. If you’re spending 60% on wants, cut it to 50%. Small wins compound. The goal isn’t to be perfect-it’s to be consistent.

Try this: For the next month, just track every dollar. Don’t change anything. Just see where your money actually goes. Then, next month, shift 5% from wants to savings. The next month, another 5%. You’ll get there.

The 30-40-30 rule isn’t about restriction. It’s about permission-to spend on what you love, to save without stress, and to stop feeling like money is always slipping through your fingers.

Final thought: It’s not about the numbers-it’s about control

Money anxiety isn’t caused by how much you earn. It’s caused by not knowing where your money goes. The 30-40-30 rule gives you a map. You don’t have to follow it exactly. But having a map means you’re never lost.

Start today. Take your last pay stub. Do the math. See where you stand. Then make one small change. That’s all it takes to begin.