Debt-to-Income Ratio Calculator

Calculate Your Eligibility

Lenders in Australia require your debt-to-income ratio to be below 40% for most personal loans. Enter your current income and debt payments to see your eligibility.

Your Debt-to-Income Ratio

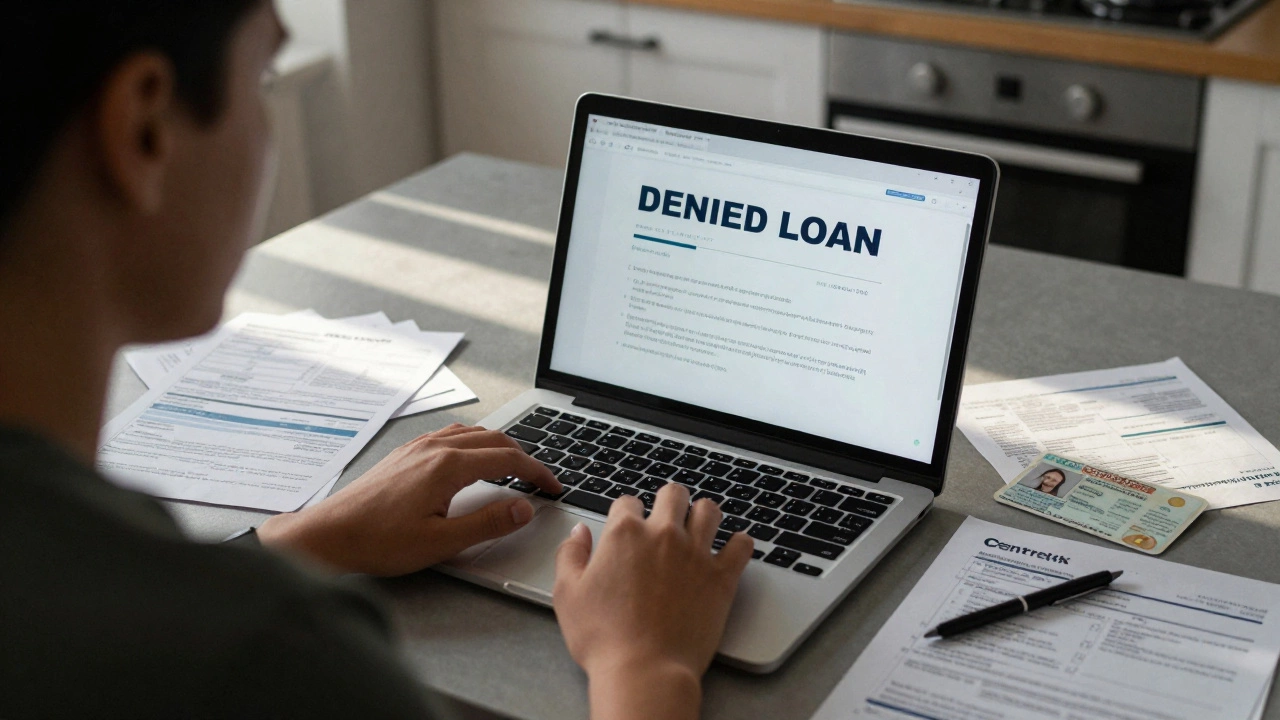

Getting a personal loan in Australia isn’t as simple as filling out a form and waiting for approval. Even if you think you’re a solid candidate, lenders have strict rules - and many people get turned down without understanding why. It’s not just about having a good credit score. There are hidden traps, overlooked details, and common mistakes that can block your application before it even gets reviewed.

Your credit score isn’t the only thing that matters

Most people assume that if their credit score is above 600, they’re safe. But lenders don’t just look at a number. They dig into your credit history. If you’ve missed payments in the last two years, had accounts sent to collections, or filed for bankruptcy, your chances drop fast. Even one late payment on a utility bill or phone contract can raise red flags if it’s recent.

In Australia, credit reporting agencies like Equifax and Illion track more than just credit cards and loans. They include mobile phone contracts, gym memberships, and even some utility bills. A default from 18 months ago can still hurt your application. Lenders don’t care if you paid it off later - the mark stays for five years.

Too much existing debt

Lenders use something called the debt-to-income ratio to decide if you can handle more debt. This isn’t just about how much you owe - it’s about how much you owe compared to how much you earn. If you’re already paying 40% or more of your take-home pay toward debts (credit cards, car loans, student loans), most lenders will say no.

For example, if you earn $65,000 a year after tax and are already paying $2,200 a month toward other debts, you’re at a 41% ratio. Even if you have a perfect credit history, that’s too high. Lenders want to see breathing room. They need to be sure you can still afford food, rent, and emergencies after making your loan payments.

Your income isn’t stable enough

Do you work freelance? Are you on a contract? Do you get paid cash-in-hand? Many lenders don’t care about how much you earn - they care about how consistent it is. If you’ve been in your current job for less than six months, or if your income varies month to month, you’ll likely be flagged.

Some lenders will accept self-employed applicants, but they’ll ask for two years of tax returns, bank statements, and proof of steady cash flow. If you’ve had a spike in income this year but your past two years were lower, you might still be denied. Lenders don’t bet on future earnings - they go by what’s already happened.

You’re applying for too much

Wanting a $30,000 loan for a $10,000 car? That’s a problem. Lenders don’t like big loans for small purchases. They’ll assume you’re using the extra cash to pay off other debts or fund risky spending. That’s a major red flag.

Even if you have the income to support it, asking for more than you need raises suspicion. A $15,000 loan for a used car might be fine. A $25,000 loan for the same car? You’ll be asked to explain where the rest will go - and if you can’t give a solid answer, your application gets rejected.

You’ve applied for too many loans recently

Applying for five different loans in three months? That’s a huge mistake. Each time you apply, the lender does a hard credit check. These show up on your report for two years. Too many in a short time make you look desperate - like you’re struggling to get approved anywhere.

Lenders see multiple applications as a warning sign. It suggests you’ve been turned down before and are now trying every option. Even if your credit is good, this pattern can trigger an automatic decline. Wait at least six months between applications if you’ve been rejected once.

You don’t have enough proof of identity or residency

This sounds basic, but it’s more common than you think. If you’ve recently moved, changed your name, or are on a temporary visa, you might be denied simply because your documents don’t match up.

Lenders need to verify you’re who you say you are. That means a current driver’s license, Medicare card, and recent utility bill with your name and address. If your driver’s license is expired, or your utility bill is from last year, or your name on your bank account doesn’t match your ID - you’ll be asked to provide more. If you can’t, your application is paused or denied.

You’re on Centrelink benefits

Many people assume Centrelink payments like JobSeeker, Youth Allowance, or Disability Support Pension are enough to qualify. They’re not. Most lenders won’t accept these as stable income. Why? Because they’re temporary, subject to change, and often don’t cover enough to reliably repay a loan.

Some lenders do offer loans for Centrelink recipients, but they’re rare. They usually come with higher interest rates, lower limits, and stricter terms. If you’re relying solely on government payments, you’ll likely be declined by mainstream lenders.

You’ve been declined before - and didn’t fix the issue

One rejection isn’t the end. But if you reapply without changing anything, you’re wasting time. If you were turned down because of high debt, and you didn’t pay anything down? You’ll be denied again. If your credit report still has defaults? Same result.

Lenders don’t change their minds unless you change your situation. Don’t just apply again. Fix the problem first. Pay off a credit card. Wait six months. Get a letter from your employer showing a raise. Update your documents. Then reapply.

What you can do instead

If you’ve been rejected, don’t panic. Start by checking your credit report for free through Equifax or Illion. Look for errors - like debts you’ve already paid off still showing as unpaid. Dispute them. They can take 30 days to fix.

Next, reduce your debt. Even paying off one credit card can lower your debt-to-income ratio enough to qualify. Try to get a pay rise, take on a side gig, or consolidate debt into a lower-interest loan.

And if you’re still stuck? Consider a guarantor loan. A family member with good credit can back your application. Or look at credit unions - they often have more flexible rules than big banks.

There’s always a way - but only if you understand why you were denied in the first place.

Can I get a personal loan with bad credit in Australia?

Yes, but it’s harder. Some lenders specialise in bad credit loans, but they charge much higher interest - often over 20% p.a. You’ll also face lower loan amounts and stricter repayment terms. Before applying, check if your credit report has errors, pay down existing debts, and consider a guarantor to improve your chances.

How long do defaults stay on my credit report?

Defaults stay on your credit report for five years in Australia, even if you pay them off. A serious credit infringement - like a court judgment - can stay for seven years. This means a missed payment from 2022 can still affect your loan application in 2026. The best move is to clear any defaults as soon as possible and ask for a ‘paid’ update on your report.

Do I need to be an Australian citizen to get a personal loan?

No, you don’t need to be a citizen. Permanent residents and some visa holders (like skilled work visa holders) can qualify. But you must prove you have stable income, a local address, and a valid ID. Temporary visa holders with short-term visas (like tourist or student visas) are usually declined because lenders can’t guarantee long-term repayment ability.

Can I get a personal loan if I’m unemployed?

It’s extremely unlikely. Lenders need proof of regular income to approve a loan. If you’re unemployed and not receiving Centrelink payments, your application will be declined. If you’re on Centrelink, some specialist lenders may approve small loans, but with high interest and low limits. Your best option is to find part-time work or a guarantor before applying.

How many loan applications can I make before it hurts my credit?

Each application triggers a hard credit check, which stays on your report for two years. Making more than two applications in six months can hurt your score and make lenders wary. If you’re shopping around, do it within a 14-day window - some lenders treat multiple checks in that time as one inquiry. Never apply for five loans in a month.