Equity Release Interest Calculator

Calculate how monthly interest impacts your lifetime mortgage debt over time. See the difference between paying interest monthly versus letting it compound.

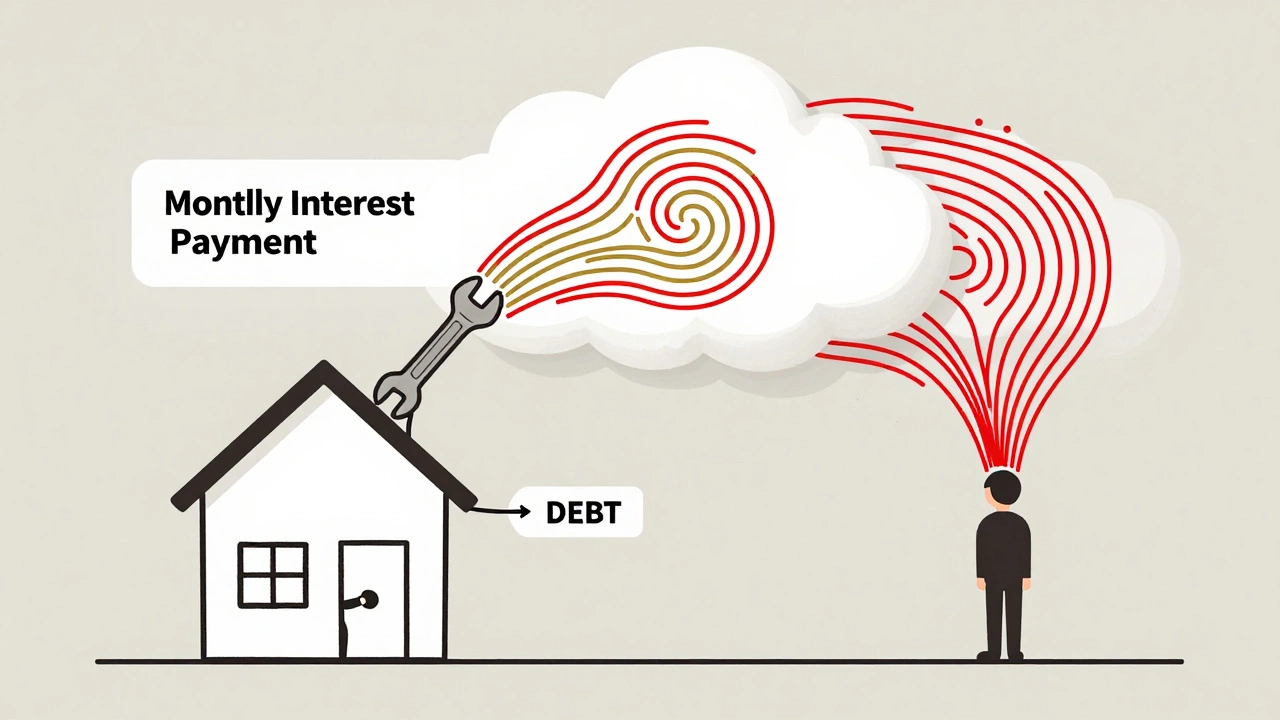

Most lifetime mortgages compound interest monthly even without monthly payments.

Your Results

Compounding EffectKey Insight:

Without monthly payments: Interest compounds monthly, causing your debt to grow significantly over time. Your home equity decreases as a result.

With monthly payments: You keep your debt stable by paying the monthly interest. This prevents compound growth and protects your home equity.

When you hear equity release, you might think of getting cash from your home without selling it. But one question keeps coming up: Do you pay monthly interest on equity release? The answer isn’t simple, and it’s not the same for everyone. Let’s cut through the confusion.

What Is Equity Release?

Equity release lets homeowners aged 55 or older unlock money tied up in their property. You don’t have to move. You don’t have to repay the loan while you live in the home. But that doesn’t mean there’s no cost. The money you get isn’t free. It’s a loan, and like any loan, it grows over time - mostly because of interest.

There are two main types: lifetime mortgages and home reversion plans. Most people choose lifetime mortgages. That’s the one where interest builds up. And yes - that interest compounds monthly.

How Interest Works on Lifetime Mortgages

With a lifetime mortgage, you borrow against your home’s value. The lender gives you a lump sum or regular payments. You don’t make monthly repayments. But the interest? It adds up - every single month.

Here’s how it works in practice:

- You borrow $150,000 at an annual interest rate of 5.8%.

- That’s 0.483% per month (5.8% divided by 12).

- After the first month, $725 in interest is added to your debt.

- Next month, interest is calculated on $150,725 - not just the original $150,000.

This is called compound interest. It doesn’t just grow slowly - it grows faster over time. After 10 years, that $150,000 could become over $250,000. After 20 years? It could be nearly $450,000. Your home’s value might rise, but so might what you owe.

Do You Ever Pay Monthly?

Most people don’t. That’s the whole point of equity release - no monthly payments. But you have choices. You can opt to pay some or all of the interest each month. If you do, you stop the debt from growing.

Let’s say you take out a $200,000 lifetime mortgage at 6% interest. Without payments, after 15 years, you’d owe roughly $480,000. But if you pay $1,000 a month in interest, you’d still owe $200,000 - the same as when you started. You’d be paying interest, but not letting it compound.

This isn’t common. Most retirees don’t have extra cash to pay monthly. But if you do - or if you’re planning to downsize later - it’s a smart move. It saves you from losing most of your home’s value to interest.

What About Home Reversion Plans?

Home reversion is different. You sell part or all of your home to a provider in exchange for cash. You keep living there rent-free. There’s no interest. No monthly payments. No compounding debt.

But here’s the catch: you give up ownership. If your home’s value doubles, the provider keeps half (or whatever share you sold). You don’t benefit from the rise. You just get the cash upfront.

So if you’re worried about interest, a home reversion plan avoids it entirely. But you’re trading future value for present cash. It’s a trade-off - not a free lunch.

Why This Matters for Retirement Planning

Many retirees use equity release to cover medical bills, home repairs, or to help family. But without understanding how interest works, you can end up with less for your heirs - or even no equity left.

According to the Equity Release Council (2025), the average lifetime mortgage balance after 12 years is 2.3 times the original amount borrowed. That’s not a typo. Two and a half times. And that’s with interest rates around 6% - not the 8% or 9% we saw in 2022.

People who don’t pay interest often assume they’ll sell the house later. But what if they can’t? What if health declines? What if the market drops? The debt doesn’t disappear. It’s paid from the sale proceeds - and whatever’s left goes to your estate. If there’s nothing left? Then there’s nothing left.

What Can You Do?

You’re not stuck with compound interest. Here are three realistic options:

- Pay interest monthly - if you have income from pensions, part-time work, or savings. This keeps your debt flat.

- Choose a capped rate plan - some lenders offer products with a maximum interest rate increase. This limits how fast your debt grows.

- Use a drawdown plan - instead of taking all the cash at once, you take it in chunks. You only pay interest on what you’ve borrowed so far. This can reduce long-term costs.

Most people don’t know these options exist. Advisors often focus on how much cash you can get - not how to protect what’s left.

What Happens When You Die or Move?

When you pass away or move into long-term care, the home is sold. The lender takes back what you owe - including all the interest that built up. Any leftover money goes to your estate.

But here’s the reality: 7 out of 10 lifetime mortgages leave nothing for heirs after 15 years, according to a 2025 study by the Australian Retirement Trust. That’s not because the homes were cheap. It’s because interest kept growing.

If you want your children to inherit something - even $50,000 - you need to plan for interest. Not ignore it.

Common Myths About Equity Release

- Myth: "You don’t pay anything until you die."

Truth: You’re paying - just not in cash. The cost is added to your debt. - Myth: "Interest rates are fixed forever."

Truth: Many are variable. They can go up. Always check the terms. - Myth: "The lender can take your home while you’re alive."

Truth: As long as you follow the rules (live in the home, keep it insured), they can’t. But if you fall behind on insurance or taxes? That’s a different story.

Final Thoughts

Yes, you pay monthly interest on equity release - even if you never see a bill. It’s built into the loan. It grows. It compounds. And unless you act, it can wipe out decades of home ownership.

Equity release isn’t bad. It’s a tool. But like any tool, it can cut you if you don’t understand how it works. If you’re considering it, ask: "What will this cost me in 10 years?" Not just "How much can I get today?"

Speak to a qualified advisor who doesn’t earn commission from the product. Ask for a projection showing how much you’ll owe after 5, 10, and 15 years. And if you can afford to pay interest monthly - do it. It’s the single best way to protect what you’ve built.