Retirement Income Calculator

How Much Do You Need to Retire Comfortably?

Based on 2025 data from the Social Security Administration and Federal Reserve

When you hear someone say they're living on their pension in the U.S., what do you picture? A comfortable life? Barely getting by? The truth is, there’s no single answer. The average pension in the USA isn’t one number-it’s a mix of Social Security, employer plans, and personal savings, and most people rely on more than one. For 2025, the numbers tell a clear story: if you’re counting on just Social Security, you’re likely to fall short of what you need to live on.

What’s the real average monthly pension in the U.S.?

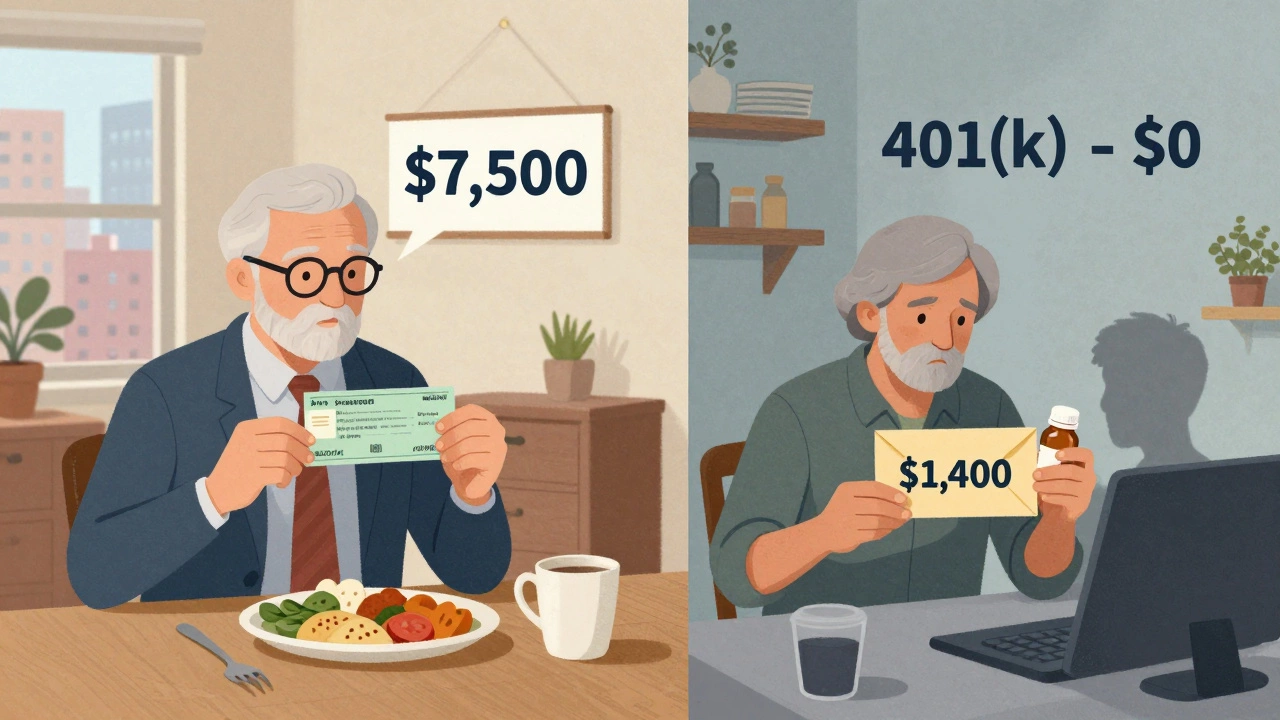

The most common source of pension-like income in the U.S. is Social Security. In 2025, the average monthly Social Security benefit for retired workers is $1,907. That’s up from $1,847 in 2024, thanks to a 2.5% cost-of-living adjustment. But here’s the catch: that’s an average. Half of recipients get less than $1,800. A quarter get under $1,400. And if you’re single and lived on a low or middle income your whole life, you’re probably in that lower half.

That $1,907 doesn’t include pensions from private employers. Only about 15% of private-sector workers have a traditional defined-benefit pension plan today. That’s down from nearly 60% in the 1980s. Most companies replaced them with 401(k) plans, where the responsibility and risk now fall on the employee.

How much do Americans actually retire with?

When you combine Social Security with other retirement income-like 401(k)s, IRAs, and part-time work-the average total monthly retirement income for Americans aged 65+ is around $4,300. That’s based on data from the Social Security Administration and the Federal Reserve’s Survey of Consumer Finances. But again, averages hide extremes.

Here’s what that looks like in real terms:

- Top 20% of retirees: $7,500+ per month

- Middle 50%: $3,000-$5,500 per month

- Bottom 20%: Under $1,800 per month

The bottom fifth? Many are living on Social Security alone. Some are working part-time. Others are depending on family support or government aid programs. The gap between those who’ve saved well and those who haven’t is growing fast.

Why is the average so low?

There are three big reasons most Americans don’t have a big pension.

First, most workers don’t have a traditional pension anymore. Even if your employer offers a 401(k), you have to contribute to it-and many don’t. A 2024 report from the Employee Benefit Research Institute found that 37% of working-age Americans have nothing saved in a retirement account. Not a dollar.

Second, even those who do save often don’t save enough. The average 401(k) balance for someone aged 65 and older is about $255,000. That sounds like a lot-until you realize it’s meant to last 20 to 30 years. If you withdraw 4% a year (a common rule of thumb), that’s just $1,020 a month. Add Social Security, and you’re at $2,900. That’s not enough to cover rent in many cities, let alone healthcare, food, and transportation.

Third, people retire earlier than they plan. Health issues, layoffs, or caregiving responsibilities force many out of the workforce before they’re ready. The median retirement age is 62, but people who retire early often have smaller savings and claim Social Security early-locking in a 30% reduction in benefits if they start at 62 instead of 67.

What’s the difference between Social Security and a pension?

People often say “pension” when they mean Social Security, but they’re not the same thing.

Social Security is a federal program funded by payroll taxes. Everyone who worked and paid into it gets a benefit based on their lifetime earnings. It’s not a savings account. You can’t withdraw it early or leave it to your kids unless they’re disabled dependents.

A true pension-also called a defined-benefit plan-is what companies used to offer. Your employer promised you a fixed monthly payment for life after you retired. The employer managed the money and took the risk. Today, only about 1 in 6 private-sector workers still have one. Government workers (federal, state, local) are more likely to have pensions, but even those are being scaled back.

Think of it this way: Social Security is like a safety net. A pension is like a paycheck that keeps coming. Most Americans today have the net, but not the paycheck.

How much should you save to replace your income?

Financial planners say you’ll need about 70% to 80% of your pre-retirement income to live comfortably. That means if you made $60,000 a year, you’ll need $42,000 to $48,000 a year in retirement.

Let’s break that down:

- Social Security (average): $22,884/year

- What you need: $45,000/year

- Gap: $22,116/year

That’s almost $2,000 a month you have to cover yourself. If you want to cover that with savings, you’d need about $500,000 invested to pull $2,000 a month safely using the 4% rule. Most people don’t have that.

And that doesn’t even include healthcare. The average 65-year-old couple retiring in 2025 will spend about $315,000 out-of-pocket on medical costs over their retirement, according to Fidelity. That’s not covered by Medicare. That’s not factored into most people’s budget.

Who has it better? Who’s struggling?

Not everyone’s in the same boat. Where you live, what you did for work, and your race and gender all affect your retirement income.

Men still get higher Social Security benefits on average because they earned more over their careers. Women are more likely to have taken time off to care for kids or elderly parents, which lowers their lifetime earnings-and their benefits.

Black and Hispanic retirees have lower average incomes than white retirees. That’s not because they didn’t work hard. It’s because of decades of wage gaps, fewer employer-sponsored plans, and less generational wealth to pass down.

And location matters. In places like San Francisco or New York City, $4,000 a month doesn’t go far. In rural Mississippi, it’s more than enough. But even in low-cost areas, inflation is eating away at fixed incomes.

What can you do if you’re behind?

If you’re in your 40s or 50s and realize you’re not on track, don’t panic. It’s not too late-but you need to act.

- Max out your 401(k). In 2025, you can contribute $23,500. If you’re 50 or older, you can add a $7,500 catch-up contribution.

- Delay Social Security. Every year you wait past 62, your benefit grows by about 8% until you hit 70. That’s a guaranteed 8% return-better than most investments.

- Work a few extra years. Even part-time work in your 60s can boost your Social Security benefit and let your savings grow longer.

- Downsize. Selling a big house and moving to a smaller one or a cheaper area can free up hundreds of thousands in equity.

- Use a reverse mortgage (carefully). It’s not a loan you repay, but it reduces your home equity. Only consider it if you plan to stay put.

There’s no magic fix. But small, consistent steps add up. Even saving an extra $200 a month from now until 65 can give you an extra $100,000 by retirement if you earn 6% annually.

What’s next for pensions in the U.S.?

Social Security is under pressure. The trust fund is projected to run out of reserves by 2034. After that, it can still pay about 80% of promised benefits using incoming payroll taxes. That means a 20% cut unless Congress acts.

Some states are trying to help. California and Oregon have created state-sponsored retirement plans for workers without employer coverage. Other states are considering similar programs. But there’s no national fix on the horizon.

The bottom line? The pension system the U.S. had in the 1970s is gone. What’s left is a patchwork of government support, employer plans, and personal savings. If you want to retire with dignity, you can’t wait for someone else to fix it. You have to build your own safety net.

What is the average monthly pension payment in the USA?

The average monthly Social Security benefit for retired workers in 2025 is $1,907. When you include other retirement income like 401(k)s and IRAs, the average total retirement income is around $4,300 per month. But half of retirees receive less than $3,000, and many rely solely on Social Security.

Is Social Security a pension?

No, Social Security is not a pension. It’s a government program funded by payroll taxes that provides monthly income based on your lifetime earnings. A pension is a private or public employer plan that pays a fixed amount each month for life. Only about 15% of private-sector workers still have a traditional pension.

How much should I save for retirement if I want to live comfortably?

To live comfortably, aim to replace 70% to 80% of your pre-retirement income. For someone earning $60,000 a year, that’s $42,000 to $48,000 annually. With Social Security covering about $22,884, you’ll need to cover the rest-around $20,000 to $25,000-from your own savings. That means having $500,000 or more saved by retirement.

Why do so many Americans have so little saved for retirement?

Many workers don’t have access to employer-sponsored retirement plans. Even when they do, they don’t contribute enough-or at all. A 2024 study found 37% of working-age Americans have zero retirement savings. Low wages, student debt, medical bills, and lack of financial education also play major roles.

Can I retire at 62 and still live well on Social Security alone?

It’s possible, but very difficult. The average Social Security benefit at age 62 is about $1,600 a month-less than the average rent in most U.S. cities. You’d need to live in a low-cost area, have no debt, and keep healthcare costs minimal. Most people who retire at 62 with only Social Security rely on family help, food assistance, or part-time work to get by.