Save $1,000 a month and you might think you’re on track to become rich. But how much will you actually have? It’s not just about adding up $1,000 every month. The real answer depends on where you put that money-and how long you leave it there.

Just Stashing Cash? You’ll Have $120,000 in 10 Years

If you stick $1,000 a month into a shoebox, a drawer, or a basic checking account with zero interest, you’ll have exactly $120,000 after 10 years. That’s $1,000 × 12 months × 10 years. Simple math. But here’s the problem: inflation eats away at that number. In 2025, $120,000 doesn’t buy what it did in 2015. The cost of housing, groceries, and healthcare has gone up. Your cash is losing value every year.

Put It in a High-Yield Savings Account? You’ll Have Around $130,000

Most people don’t just leave money sitting idle. The smart move is to put it in a high-yield savings account. As of December 2025, the average APY (annual percentage yield) for these accounts is 4.25%. Some online banks offer 4.5% or even 5% if you meet minimum balance requirements.

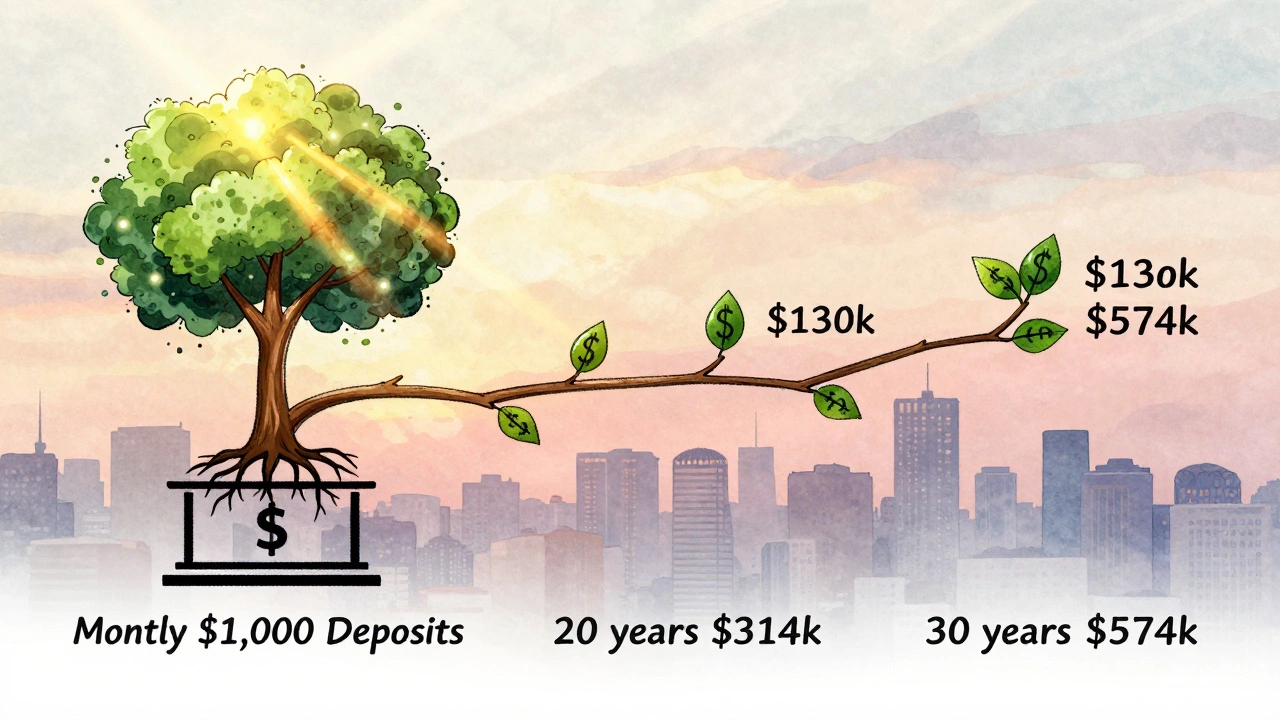

With a 4.25% APY, saving $1,000 a month for 10 years gives you $130,758. That’s $10,758 in interest earned-just from letting your money sit and grow. It’s not life-changing, but it’s better than nothing. The key? You need to pick a real high-yield account, not the one at your local bank that pays 0.01%.

What If You Save for 20 Years? Over $300,000

Time is your best friend when it comes to saving. Stretch that $1,000-a-month habit to 20 years, and with the same 4.25% APY, you’ll end up with $314,725. That’s more than double what you’d put in. The interest compounds because each month’s deposit earns interest, and then next month’s interest is calculated on a slightly bigger balance.

After 30 years? You’ll have $574,200. That’s half a million dollars built from just $360,000 of your own money. The rest? Pure compound growth.

Compare: Savings Account vs. CD vs. Money Market

Not all savings tools are the same. Here’s how they stack up with $1,000 a month saved at current 2025 rates:

| Account Type | Typical APY | 10-Year Total | Interest Earned |

|---|---|---|---|

| Basic Checking Account | 0.01% | $120,012 | $12 |

| High-Yield Savings | 4.25% | $130,758 | $10,758 |

| Money Market Account | 4.35% | $131,215 | $11,215 |

| 10-Year CD (laddered) | 4.50% | $132,142 | $12,142 |

Money market accounts are similar to high-yield savings but often let you write checks or use a debit card. CDs lock your money for a set term-like 1, 3, or 5 years-but pay slightly more. If you ladder them (open new CDs every few months), you get flexibility and better rates.

Why Not Just Invest in the Stock Market?

You might hear people say, "Just invest in index funds instead." And they’re right-if you’re willing to take risk. The S&P 500 has returned about 10% annually over the last 30 years. If you invested $1,000 a month into an S&P 500 index fund at that rate, you’d have $196,800 in 10 years. That’s $76,000 more than in a savings account.

But here’s the catch: markets go down. In 2022, the S&P 500 dropped 19%. If you saved $1,000 a month during that year and your portfolio lost 15% in December, you’d feel the pain. Savings accounts don’t do that. Your balance never goes negative. No one wakes up wondering if their emergency fund vanished overnight.

So savings accounts are for safety. Investing is for growth. You need both.

What’s the Right Strategy?

Here’s what works for most people:

- Keep 3-6 months of living expenses in a high-yield savings account. That’s your safety net.

- Save $1,000 a month toward a specific goal: a house down payment, a car, a wedding, or a medical fund.

- Once you hit that goal, move the money into something with higher growth potential-like a brokerage account.

- For long-term goals (retirement, kids’ college), invest. For short-term goals (under 5 years), keep it in savings.

Don’t try to make your emergency fund grow like a stock portfolio. If you need that money in six months and the market crashes, you’re stuck selling low.

Real-Life Example: Sarah’s $1,000-a-Month Plan

Sarah, 28, makes $55,000 a year. She sets up automatic transfers: $1,000 goes into her high-yield savings account the day after payday. She’s saving for a house and wants $50,000 for a down payment in 4 years.

After 4 years, she’ll have $49,700-with $1,700 in interest. She also added $20,000 from her tax refund and a small inheritance. She’s on track.

She didn’t get rich. But she didn’t stress either. She bought her first home at 32 without debt.

Common Mistakes People Make

- Waiting until they "have more money" to start saving. Starting with $1,000 a month now beats waiting for $2,000 a month later.

- Using a bank that pays less than 0.5% APY. You’re throwing away hundreds over time.

- Not automating it. If you have to remember to transfer money, you’ll forget.

- Trying to chase the highest rate without checking fees or withdrawal limits.

- Mixing short-term savings with long-term investing. Don’t put your vacation fund in stocks.

How to Get Started Today

You don’t need a financial advisor to make this work. Here’s what to do right now:

- Open a high-yield savings account at Ally, Marcus, or Capital One. They’re FDIC-insured and pay 4.25%+.

- Set up an automatic transfer of $1,000 from your checking account on the same day you get paid.

- Label the account clearly: "House Down Payment 2028" or "Emergency Fund"-so you don’t accidentally spend it.

- Check your balance every 3 months. Celebrate milestones. $10,000 saved? Treat yourself to a nice dinner. $50,000? Book a trip.

It’s not glamorous. But it’s powerful. People who save $1,000 a month consistently are in the top 10% of American savers. You don’t need to earn six figures. You just need to be consistent.

How much will I have if I save $1,000 a month for 5 years?

At a 4.25% APY, saving $1,000 a month for 5 years gives you $63,482. That includes $3,482 in interest. Without interest, you’d have $60,000.

Can I save $1,000 a month on a $50,000 salary?

Yes, but it takes discipline. $1,000 a month is 24% of your take-home pay after taxes. You’ll need to cut non-essentials, cook at home, avoid subscriptions you don’t use, and track every dollar. It’s hard at first, but most people find they can do it after 3-6 months of budgeting.

Should I save $1,000 a month or invest it instead?

It depends on your timeline. If you need the money in less than 5 years, save it. If it’s for retirement or 10+ years away, invest. For most people, the best approach is to do both: save for short-term goals, invest for long-term ones.

What’s the best bank for saving $1,000 a month?

Online banks like Ally, Marcus by Goldman Sachs, and Capital One offer the highest rates-usually 4.25% to 5%. They have no monthly fees, no minimum balance, and easy mobile access. Avoid big-name brick-and-mortar banks-they typically pay under 0.1%.

How does inflation affect my savings?

Inflation reduces your purchasing power. If inflation is 3% a year, your $130,000 in 10 years will only have the buying power of about $97,000 today. That’s why it’s smart to move savings into higher-growth investments over time-especially for goals 10+ years away.

Is it better to save $1,000 a month or $30,000 once a year?

Monthly savings win because of compounding. Even with the same total amount, $1,000 a month earns more interest than $30,000 once a year. The first $1,000 you save in January earns interest for 11 months. The last $1,000 in December earns almost none. But the annual lump sum earns zero interest until it’s deposited.

Final Thought: It’s Not About the Money. It’s About the Habit.

People who save $1,000 a month aren’t necessarily the highest earners. They’re the ones who made saving non-negotiable. They didn’t wait for motivation. They built a system.

That system-automatic transfers, a high-yield account, clear goals-is what turns $1,000 a month into financial freedom. Not magic. Not luck. Just consistency.