Remortgage Comparison Calculator

Compare your current mortgage with potential new offers to see if switching lenders saves you money. Based on data from the Australian Competition and Consumer Commission.

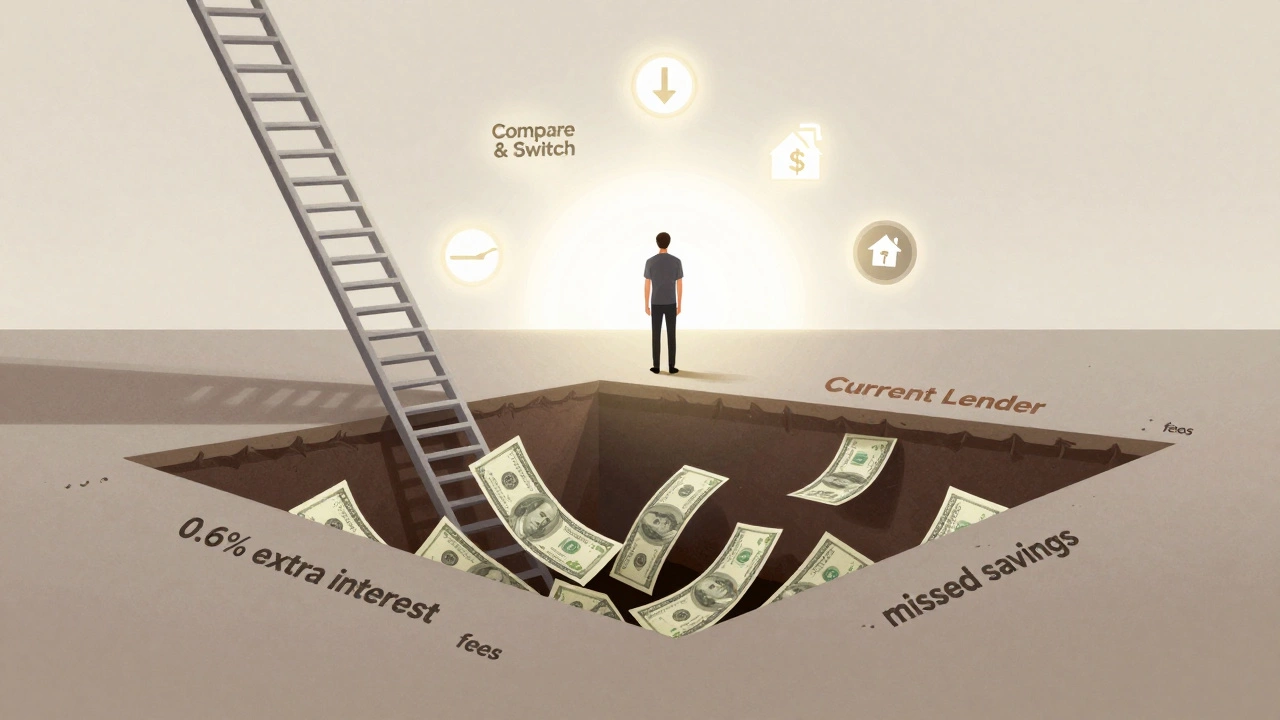

Based on the Australian Competition and Consumer Commission data: Customers who stayed with their existing lender paid an average of 0.6% more in interest than those who switched. On a $700,000 mortgage, this equals $4,200 extra per year.

Source: ACCC (2025)

When you’re thinking about remortgaging, one of the first questions that comes up is: should I stick with my current lender? It feels safer, right? You already know them. You’ve sent them your payslips, answered their questions, and maybe even had a friendly chat with their customer service rep. But does familiarity actually save you money - or are you missing out on something better?

Why people consider staying with their current lender

Staying with your existing lender sounds convenient. You don’t have to fill out a new application from scratch. Your financial history is already in their system. There’s no need to gather bank statements or proof of income again. For many, that ease is tempting - especially if you’re busy, stressed, or just tired of paperwork.

Some lenders even offer a ‘loyalty discount’ or a streamlined process for existing customers. You might get faster approval, or they might waive certain fees like valuation or legal costs. In Australia, some banks like Commonwealth Bank, NAB, or ANZ have internal refinancing teams that handle these requests quickly. But here’s the catch: those perks are rarely enough to beat what’s out there.

The real cost of staying put

Most people don’t realize how much they’re paying just because they didn’t shop around. The average homeowner in Australia stays with their lender for over 7 years. During that time, interest rates change. New products launch. Competitors offer better deals just to lure in customers like you.

In early 2025, the Reserve Bank of Australia held rates steady after a series of hikes, but lenders still competed fiercely for borrowers. One study from the Australian Competition and Consumer Commission (ACCC) found that customers who stayed with their existing lender paid an average of 0.6% more in interest than those who switched. That might not sound like much, but on a $700,000 mortgage, it adds up to over $4,200 extra per year.

And it gets worse. If your current lender doesn’t actively compete - and many don’t - you could be stuck on a standard variable rate when you could be on a discounted fixed rate with better features. Some lenders even push customers onto their most expensive product after a fixed term ends, assuming they won’t bother to switch.

What you might be missing

When you look beyond your current lender, you open up options you didn’t even know existed. Smaller banks and non-bank lenders (like ME Bank, Pepper, or Liberty) often have lower rates and fewer restrictions. They don’t have branches everywhere, so they cut costs elsewhere - and pass those savings to you.

For example:

- You might get a loan with offset accounts that actually reduce your interest - something your current lender charges extra for.

- Some lenders offer portability - letting you take your loan with you if you move house - without extra fees.

- Others give you free redraw access or allow you to make extra repayments without penalties.

And then there’s the negotiation factor. If you tell your current lender you’re thinking of switching, they might offer you a better deal just to keep you. But don’t expect them to lead with it. You have to ask. And you need to know what’s out there first.

When staying makes sense

There are times when staying put is the smart move. If you’re on a fixed-rate loan that ends in 6 months, and current market rates are higher than what you’re paying, it might not make sense to switch. Locking in now could cost you more in the long run.

Also, if you’ve got a low loan-to-value ratio (LVR) - say, under 60% - you’re in a strong position. Your lender knows you’re low-risk. That gives you leverage. You can use that to negotiate a better rate without leaving.

And if you’ve got a complex financial situation - like being self-employed, having multiple properties, or a recent credit event - your current lender already understands your history. Switching might mean starting over with new documentation, new assessments, and a higher chance of rejection.

How to compare properly

You don’t need to switch. But you should compare. Here’s how to do it right:

- Check your current rate and fees. Look at your latest statement. What’s your actual interest rate? Are you paying monthly service fees, annual fees, or early repayment charges?

- Use a mortgage comparison tool. Sites like RateCity or Canstar show live rates from dozens of lenders. Filter for loans with the same features as yours - offset accounts, redraw, etc.

- Call 3-5 lenders. Ask: “If I was switching from [your current lender], what rate could you offer me?” Don’t say you’re already a customer. That way, you get the real market rate.

- Calculate the break-even point. Add up all the costs of switching - application fees, valuation fees, legal fees. Then divide that by how much you’d save each month. If it takes more than 12 months to break even, it might not be worth it.

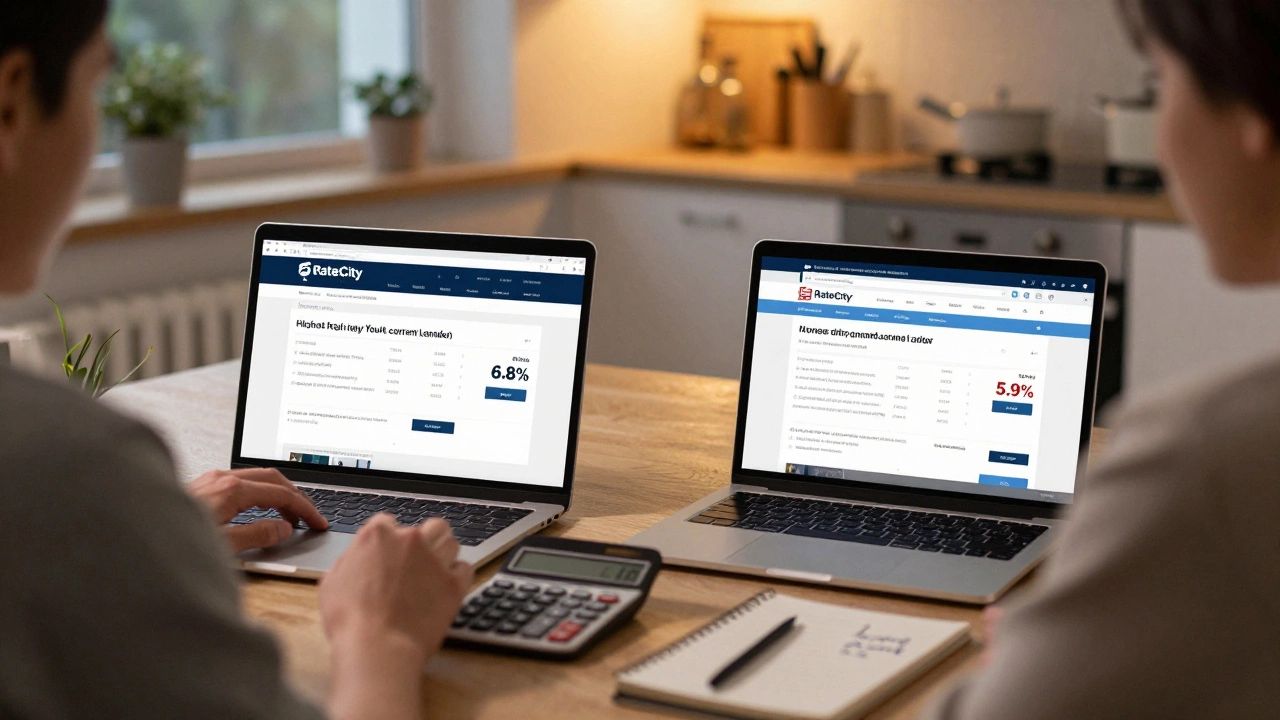

One Sydney homeowner did this in late 2025. She was paying 6.8% on her $650,000 loan. After comparing, she found a lender offering 5.9% with no fees. She saved $520 a month. The switching costs? $1,800. She broke even in 3.5 months.

The hidden trap: loyalty isn’t rewarded - it’s exploited

Many lenders count on you not switching. They assume you’re too busy, too tired, or too scared to change. So they don’t compete for you. They just let you sit there, paying more.

There’s no legal requirement for lenders to offer loyal customers the best rates. In fact, research from the University of Sydney’s Centre for Financial Studies found that customers who never switched paid up to 18% more over 10 years than those who switched every 2-3 years.

Think of it like this: if you never changed your mobile plan, you’d still be paying $120 a month for a $40 plan. That’s what’s happening with your mortgage.

What to do next

Don’t wait for your lender to contact you. Don’t assume they’ll give you a better deal. Take 20 minutes today.

- Log into your online banking and note your current rate and fees.

- Go to RateCity or Canstar and enter your loan details.

- Find one or two offers that look better.

- Call your lender. Say: “I’ve seen a better deal elsewhere. Can you match it?”

If they say no - or give you a half-hearted offer - switch. The process takes 3-6 weeks. Most lenders handle the paperwork. You don’t need to change banks. You just need to change your loan.

And remember: this isn’t about being disloyal. It’s about being smart. Your mortgage is the biggest financial decision you’ll make. Treat it like one.

Is it cheaper to remortgage with my current lender?

Not usually. While staying with your current lender might save you some paperwork or fees, it rarely saves you money on interest. Most lenders don’t automatically give loyal customers the best rates. In fact, many Australians pay hundreds more per year simply because they didn’t shop around. Always compare rates from at least three lenders before deciding.

Can I negotiate a better rate with my existing lender?

Yes - but only if you’re prepared to walk away. Lenders are more likely to offer a better rate if you tell them you’re considering switching. Have concrete numbers ready: show them a competitor’s offer with a lower rate and similar features. Be polite but firm. Many lenders will match or beat it just to keep you.

What are the costs of switching lenders?

Switching lenders can cost between $1,500 and $4,000, depending on your situation. Common fees include application fees ($300-$600), valuation fees ($200-$500), legal fees ($500-$1,000), and discharge fees from your current lender ($150-$350). Some lenders waive these fees to attract new customers. Always ask for a full fee breakdown before proceeding.

How often should I consider remortgaging?

Every 2-3 years is a good rule of thumb. Interest rates change frequently, and lenders regularly launch new products with better terms. If you’ve been with the same lender for more than 3 years, you’re likely paying more than you need to. Even if you’re on a fixed rate, check your options before the term ends.

Will switching lenders affect my credit score?

A single application for a new mortgage won’t hurt your credit score significantly. Lenders perform a hard credit check, which may lower your score by a few points temporarily. But if you apply to multiple lenders within a 30-day window, most credit agencies treat it as one inquiry. Just avoid applying to more than 3-4 lenders to stay safe.