70-10-10-10 Budget Calculator

Enter your net pay (after tax).

Ready to plan?

Enter your income to see how the 70-10-10-10 rule applies to you.

Have you ever looked at your bank account and wondered where all your money went? You’re not alone. Most people struggle with keeping track of their expenses because traditional budgeting feels too rigid or complicated. That’s why many are turning to the 70-10-10-10 budget rule. It’s a flexible framework that helps you allocate your income into four clear categories without feeling like you’re on a strict diet.

This method isn’t just about cutting back; it’s about balancing your needs, wants, savings, and debt repayment in a way that fits your lifestyle. Whether you’re living in Sydney, managing student loans, or saving for a house deposit, this rule offers a practical path forward. Let’s break down how it works and why it might be the missing piece in your financial puzzle.

Understanding the 70-10-10-10 Framework

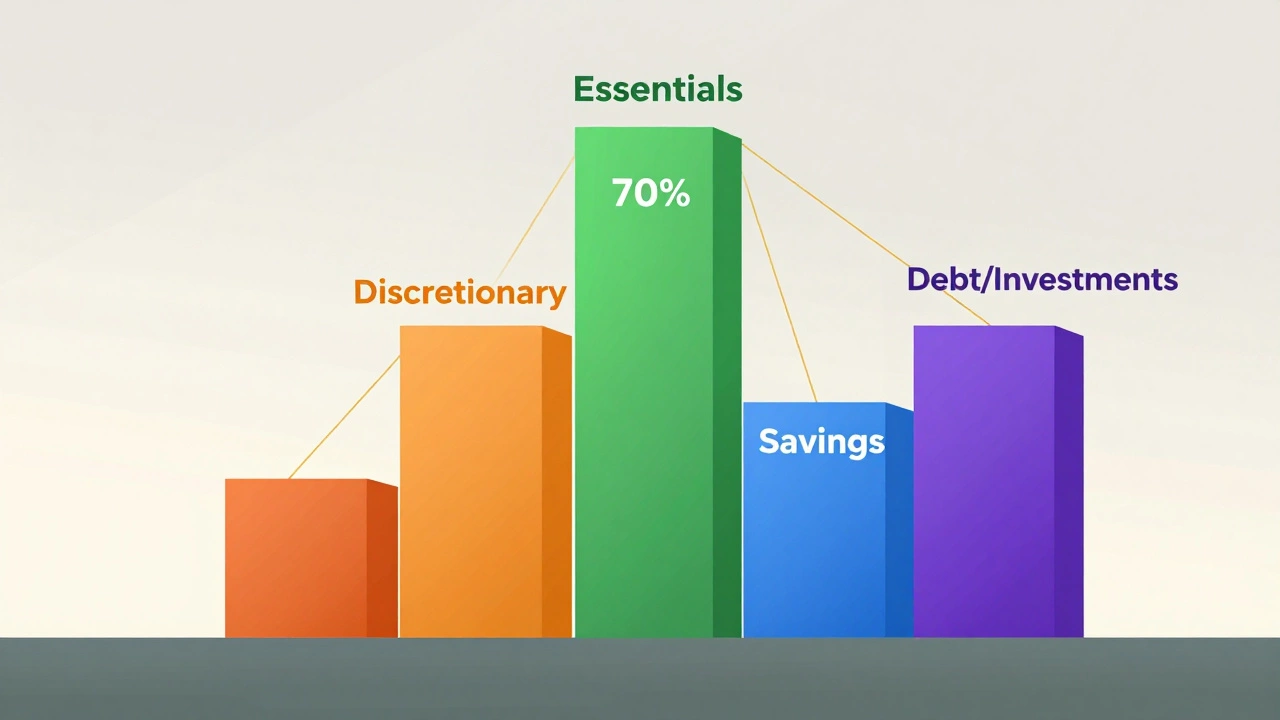

The 70-10-10-10 budget rule divides your after-tax income into four buckets: 70% for essentials, 10% for discretionary spending, 10% for savings, and 10% for debt repayment or investments. Unlike the popular 50/30/20 rule, which groups everything into three broad categories, this approach separates savings and debt/investment goals. This distinction matters because it forces you to prioritize both building wealth and clearing liabilities simultaneously.

| Category | Percentage | Purpose |

|---|---|---|

| Essentials | 70% | Rent, groceries, utilities, transport |

| Discretionary | 10% | Dining out, hobbies, entertainment |

| Savings | 10% | Emergency fund, short-term goals |

| Debt/Investments | 10% | Credit card payments, superannuation, stocks |

The beauty of this system lies in its simplicity. You don’t need spreadsheets or complex apps to get started. Just divide your monthly take-home pay by ten, then multiply accordingly. For example, if you earn $5,000 per month after tax, $3,500 goes to essentials, $500 to fun stuff, $500 to savings, and $500 to paying off debts or investing. It’s straightforward enough to stick with even when life gets busy.

Why the 70-10-10-10 Rule Works Better Than Traditional Methods

Traditional budgeting often fails because it relies on willpower rather than structure. The 70-10-10-10 rule removes guesswork by assigning specific roles to each portion of your income. Here’s why it stands out:

- Clarity: Each category has a defined purpose, so there’s no confusion about whether a coffee shop visit counts as "needs" or "wants."

- Flexibility: If your rent increases, you can adjust within the 70% bucket without derailing other priorities.

- Balanced Growth: By separating savings and debt repayment, you avoid neglecting one area while focusing on the other.

Consider Sarah, a graphic designer earning $6,000 monthly. She used to throw all her extra cash into an emergency fund but ignored her credit card balance. With the 70-10-10-10 rule, she now allocates $600 toward reducing her debt while still contributing $600 to her high-interest savings account. Over time, this dual focus improved her credit score and gave her peace of mind during unexpected expenses.

How to Apply the Rule in Real Life

Implementing the 70-10-10-10 budget rule doesn’t require perfection from day one. Start by calculating your net income-the amount left after taxes and deductions. Then categorize your current spending to see where things stand. Use bank statements or budgeting apps like YNAB (You Need A Budget) or EveryDollar to identify patterns.

- List all fixed costs such as rent, mortgage, insurance premiums, and minimum loan payments. These fall under the 70% essentials category.

- Add variable costs like groceries, public transport fares, and household supplies. Keep these totals below 70% combined with fixed costs.

- Set aside 10% for guilt-free indulgences. Think movie tickets, gym memberships, or weekend trips. Without this slice, burnout becomes likely.

- Automate transfers for the remaining two 10% portions. Direct deposits into separate accounts ensure consistency and reduce temptation.

If your numbers don’t add up initially, tweak them gradually. Maybe you’ll cut cable TV to free up space for higher savings contributions. Or perhaps refinancing a car loan lowers your essential expenses enough to boost investment allocations. Small changes compound over months and years.

Common Mistakes to Avoid

Even simple systems have pitfalls. One common error is misclassifying expenses. For instance, treating streaming services as "essentials" instead of "discretionary" skews your ratios. Another mistake is ignoring inflation. What fits comfortably in 70% today may stretch thin tomorrow if prices rise significantly.

Also beware of lifestyle creep. As incomes grow, people tend to increase spending across the board. Resist upgrading every expense proportionally. Instead, channel raises directly into savings or debt reduction until those buckets reach comfortable levels.

Lastly, don’t forget to review regularly. Life events-marriage, childbirth, job loss-demand adjustments. Revisit your budget quarterly to align with changing circumstances.

Tailoring the Rule to Your Situation

No single formula suits everyone perfectly. High-cost cities like Sydney might push essentials closer to 80%, leaving less room elsewhere. In such cases, consider temporarily shifting some discretionary funds toward housing stability. Conversely, someone without debt could redirect their 10% allocation entirely into investments or early retirement planning.

Freelancers face unique challenges due to irregular earnings. They should base calculations on average monthly income rather than peak months. Building a buffer fund first ensures smoother transitions between lean periods and profitable ones.

Parents juggling childcare costs may find the standard split unrealistic. Adjust percentages based on family size and dependency needs. Prioritize education savings alongside everyday necessities to secure long-term outcomes.

Tools to Help You Stay On Track

Technology makes sticking to any budget easier. Apps like Mint, PocketGuard, or Even provide real-time insights into spending habits. Set up alerts for approaching limits in each category. Visual dashboards help spot trends quickly.

Bank accounts play a crucial role too. Open dedicated subaccounts for savings and debt repayment. Name them clearly-"Emergency Fund," "Car Loan Payoff," etc.-to reinforce intent. Some banks offer automatic rounding features that funnel spare change into targeted pots effortlessly.

For visual learners, create charts or graphs showing progress toward milestones. Celebrating small wins keeps motivation high. Did you pay off $1,000 of credit card debt? Treat yourself modestly within the 10% discretionary allowance.

FAQs About the 70-10-10-10 Budget Rule

Is the 70-10-10-10 rule better than the 50/30/20 rule?

It depends on your priorities. The 50/30/20 rule combines savings and debt into one 20% bucket, which works well for beginners. However, the 70-10-10-10 rule provides more granularity by splitting savings and debt/investments. This separation encourages balanced growth and prevents neglecting either goal.

Can I use this rule if I’m self-employed?

Yes, but adapt it carefully. Base calculations on average monthly income rather than fluctuating highs and lows. Build a reserve fund equivalent to three to six months’ worth of expenses before fully committing to the rule. Automate transfers whenever possible to maintain discipline despite inconsistent cash flow.

What happens if my essentials exceed 70%?

Adjust temporarily. Reduce discretionary spending or pause non-critical investments until essentials stabilize. Explore ways to lower fixed costs, such as negotiating bills, downsizing accommodations, or consolidating loans. Once stabilized, return to the original ratio.

Should I include taxes in the 70-10-10-10 calculation?

No, always start with after-tax income. Taxes are unavoidable obligations deducted automatically, so they shouldn’t factor into discretionary allocations. Focus solely on what remains available for spending, saving, and investing.

How do I handle irregular expenses like annual insurance premiums?

Divide large periodic payments by twelve and set aside that amount monthly. For example, a $1,200 yearly car registration translates to $100 saved each month. Include these amounts in the 70% essentials category to prevent surprises later.

Does this rule work for couples sharing finances?

Absolutely. Combine incomes and apply the rule collectively. Alternatively, manage individual budgets separately using proportional shares. Communication is key-discuss shared goals, responsibilities, and preferences openly to avoid conflicts.

What if I want to save more than 10%?

Feel free to shift percentages according to your objectives. Increase savings to 20% or 30% if accelerating home ownership or retirement plans. Compensate by trimming discretionary spending or optimizing essential costs through smarter choices.

Are there apps specifically designed for the 70-10-10-10 rule?

While no app caters exclusively to this model, most modern budgeting tools allow custom categories. Configure yours to match the four segments easily. Popular options includeYNAB, Goodbudget, and Spendee, which support personalized setups seamlessly.