Home Insurance Savings Calculator

Estimate potential savings when switching home insurance providers. Enter your current and new policy details to see your projected annual savings and identify potential coverage risks.

When you hear the word "switch" most people picture a massive hassle, but changing your home insurance can actually be a smooth, almost painless process if you know the right steps. In Australia, you don’t need a medical exam, you’re not locked into a multi‑year contract, and the law even gives you a 14‑day cooling‑off period. This guide walks you through everything you need to know, from spotting the right deal to making sure the hand‑over between insurers is crystal clear.

Quick Takeaways

- Switching home insurance usually takes 2‑4 weeks from start to finish.

- You can compare quotes online for free and still keep your current cover until the new policy starts.

- Look out for cancellation fees, lapse of cover, and any differences in deductible.

- The 14‑day cooling‑off period protects you if the new policy isn’t what you expected.

- Use the Australian Financial Complaints Authority (AFCA) if disputes arise during the switch.

What Exactly Is Home Insurance?

Home Insurance is a type of property insurance that protects your residence against damage, theft, fire, natural disasters, and liability claims. It typically covers the building (walls, roof, fixtures) and may also include contents, which are the belongings inside the home.

Why People Consider Switching

Most homeowners start thinking about a change when they spot a cheaper premium, notice a gap in coverage, or simply want better service. In recent years, online comparison tools have made it easier to spot savings of up to 15‑20 % compared to legacy insurers. Additionally, life events - buying a new house, major renovations, or adding a pool - often trigger a reassessment of coverage needs.

Key Players in the Switching Process

Understanding the roles each entity plays helps you avoid surprises.

- Insurance Provider is the company that underwrites and issues your home insurance policy. This could be a large national insurer or a niche specialist.

- Policy is the legal contract that outlines your coverage, premiums, deductibles, and exclusions. Each insurer names theirs differently-"Standard Home Cover" vs "Premium Home Shield", for example.

- Premium is the amount you pay (usually annually or monthly) to keep the policy active. It’s influenced by location, building materials, and claims history.

- Deductible is the out‑of‑pocket amount you agree to pay when you make a claim. Higher deductibles often lower the premium.

- Coverage is the scope of protection, including building, contents, and liability. Some policies also add optional extensions like flood or earthquake cover.

- Claims is the process you follow to request payment after a loss. Fast claim handling is a top factor for many buyers.

- Australian Financial Complaints Authority (AFCA) is the external dispute‑resolution body that helps resolve conflicts between consumers and insurers. It’s free to use and can intervene if the switch goes wrong.

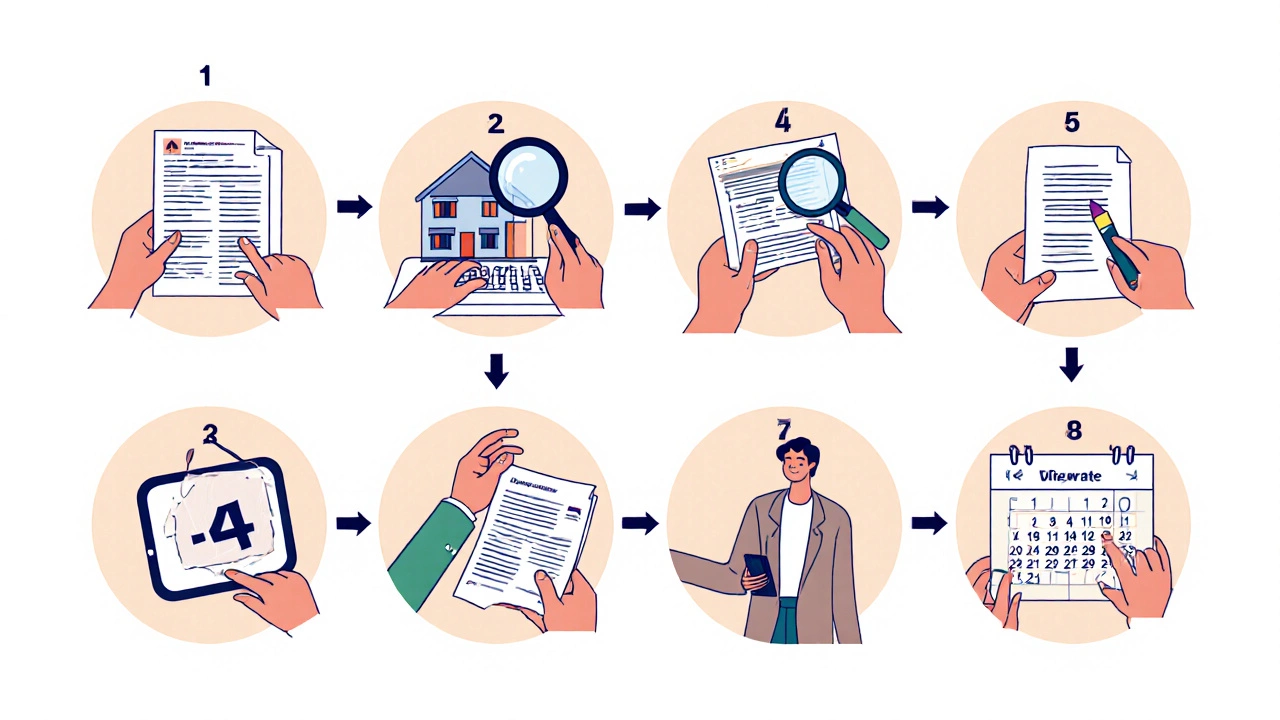

Step‑by‑Step: How to Switch Home Insurance

- Gather your current policy details. Log into your insurer's portal or pull the insurance certificate. Note the policy number, expiry date, coverage limits, and deductible.

- Run a quick coverage audit. Ask yourself: Do I need higher building coverage after recent renovations? Is my contents limit enough for new electronics?

- Shop around using comparison sites. Websites like iSelect, Compare the Market, and Finder allow you to input address, rebuild cost, and desired cover. Aim for at least three quotes.

- Check the fine print. Look for exclusions (e.g., bushfire in certain zones), premium increase caps, and whether discounts are applied for bundling with car insurance.

- Contact the new provider. Request a formal quote and ask for a written policy draft. Confirm the start date - it should be after your current policy’s expiration to avoid a coverage gap.

- Arrange the hand‑over. Once you accept the new quote, the new insurer will usually issue a “Letter of Acceptance”. Provide this to your current provider and ask them to cancel effective the day after the new policy starts.

- Take advantage of the cooling‑off period. Australian law gives you 14 days after acceptance to cancel without penalty. Review the new policy documents carefully during this window.

- Pay the first premium. Most insurers allow a one‑off payment or split into monthly installments. Set up automatic payments to avoid missed premiums.

- Confirm cancellation. Request a confirmation letter from your old insurer. Keep it for records; some providers issue a small cancellation fee, but it’s usually refundable if you cancel early.

Checklist: Things to Verify Before You Switch

- Exact rebuild cost for your area (use local council data).

- Discount eligibility (no‑claims, multi‑policy, loyalty).

- Deductible levels that match your budget.

- Coverage for specific risks (bushfire, hail, flood).

- Terms for early cancellation fees on the current policy.

- Confirmation of the 14‑day cooling‑off period.

- AFCA registration of both insurers (ensures you can lodge a complaint).

Common Pitfalls and How to Avoid Them

Gap in coverage. If your new policy starts a day after the old one ends, you might be uncovered for a night. Align dates exactly.

Hidden fees. Some insurers charge a $80 administration fee for early cancellation. Ask for a fee breakdown before you sign.

Incorrect rebuild cost. Under‑insuring can leave you paying out‑of‑pocket after a disaster. Use a professional estimator if you’re unsure.

Missing endorsements. If you have a pool, out‑building, or home office, make sure these are added to the new policy.

Assuming the cheapest is best. Low premiums often mean higher deductibles or limited claim support. Read customer reviews on claim turnaround time.

Pro Tips for a Seamless Switch

- Ask the new insurer to handle the cancellation for you. Some providers will take care of it as part of the onboarding service.

- Keep copies of all correspondence-email confirmations, letters of acceptance, and cancellation notices.

- Set a calendar reminder for the premium due date of the new policy.

- If you’re bundling with car or contents insurance, re‑evaluate those covers too-sometimes a new bundle offers extra savings.

- Use the AFCA website to check each insurer’s complaint resolution record before you commit.

Cost Savings: Real‑World Example

Emma, a homeowner in Sydney’s Eastern Suburbs, paid $1,800 per year for a standard 20‑year‑old policy. After using a comparison tool, she found a newer insurer offering the same building cover for $1,440 and a lower deductible. By switching, she saved $360 annually-enough to fund a small bathroom remodel. The switch took 21 days, and the insurer handled the cancellation at no extra cost.

When It Might Be Better Not to Switch

If you have a long‑standing claim‑free record, some insurers give you a “no‑claims bonus” that can be worth 10‑15 % discount. Breaking that relationship could reset the bonus. Also, if you’re in the middle of a major renovation, staying with a provider that already knows your property’s specifics may avoid re‑assessment costs.

Frequently Asked Questions

Frequently Asked Questions

How long does the whole switching process usually take?

From gathering quotes to final cancellation, most homeowners finish in 2‑4 weeks. The longest part is waiting for your new insurer to issue the Letter of Acceptance.

Will I lose my no‑claims discount if I switch?

No. In Australia, the no‑claims discount is a personal factor that moves with you. Just make sure the new insurer accepts it during underwriting.

Do I need to notify my mortgage lender?

Most lenders require you to keep adequate building cover at all times. Inform them of the new policy’s start date and provide a copy of the certificate.

What if the new policy has a higher deductible?

A higher deductible reduces your premium, but you’ll pay more out‑of‑pocket on a claim. We recommend matching the deductible to what you could comfortably afford in an emergency.

Can I switch if I have an ongoing claim?

It’s possible, but most insurers prefer to settle the current claim before you move. Canceling mid‑claim can complicate payouts, so finish the claim first or discuss the transition with both providers.

Bottom Line

Changing home insurance isn’t the nightmare many imagine. With the right preparation-knowing your current coverage, comparing quotes, aligning dates, and using the cooling‑off period-you can lock in better rates and tighter protection in just a few weeks. Keep the checklist handy, verify the new insurer’s AFCA record, and you’ll glide through the switch with confidence.