Equity Release Calculator

Calculate Your Equity Release Options

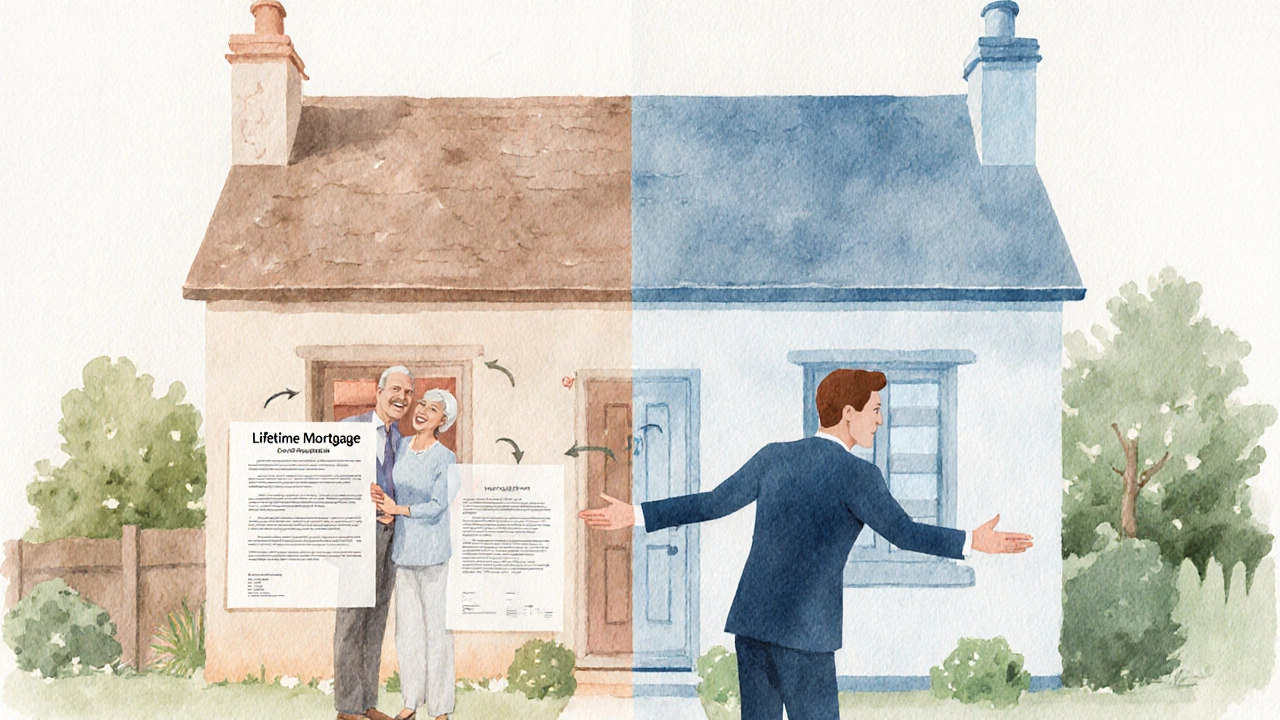

Your Equity Release Options

Lifetime Mortgage

Home Reversion

When you hear the term equity release, you might picture seniors digging out the hidden cash in their homes. But not every homeowner fits the bill, and not every plan works the same. This guide breaks down who really benefits from equity release, what factors to weigh, and how to spot the right product for your situation.

Key Takeaways

- Equity release suits owners aged 55+ with substantial home value and limited debt.

- Lifetime mortgages are best for those who want to stay in their home while borrowing against its value.

- Home reversion works well for owners who need a large lump sum and are comfortable selling a share of the property.

- Financial advisors play a crucial role in matching the product to personal cash‑flow needs.

- Always run the numbers: interest accrual, repayment scenarios, and impact on pensions.

Understanding Equity Release

Equity Release is a financial arrangement that allows homeowners, typically over 55, to access the cash tied up in their property without having to move. In Australia, the two most common products are lifetime mortgages and home reversion plans. Both let you tap into home equity, but they differ in ownership, repayment, and risk.

Who Should Consider Equity Release?

Not everyone over 55 needs or should use equity release. Below are the profiles that usually get the most benefit.

- Age‑eligible homeowners who are 55 or older and plan to stay in the house for at least a decade.

- High‑value property owners with a market value of at least $600,000, giving enough equity to borrow against.

- Low‑debt borrowers whose mortgage balance is low relative to the home’s value, keeping the debt‑to‑income ratio manageable.

- Retirees with limited pension income who need a cash boost for medical costs, home renovations, or to improve lifestyle.

- Couples seeking to stay together but want to avoid selling the family home.

Key Factors to Evaluate

Before jumping in, run through these checkpoints.

- Age eligibility: Most providers set the minimum at 55, but interest rates often improve after 65.

- Property value: Lenders typically allow borrowing up to 50‑60% of the appraised value.

- Existing mortgage balance: The lower the existing debt, the more you can unlock.

- Interest structure: Lifetime mortgages accrue interest daily; home reversion has no interest but reduces future inheritance.

- Impact on pensions and benefits: Large lump sums can affect Centrelink entitlements.

- Regulatory oversight: In Australia, the Australian Prudential Regulation Authority (APRA) provides guidelines to protect borrowers.

Lifetime Mortgage vs. Home Reversion

Choosing the right product hinges on how you want to retain ownership and how you plan to manage interest.

| Feature | Lifetime Mortgage | Home Reversion |

|---|---|---|

| Ownership | You keep 100% ownership; loan is secured against the home. | You sell a share (usually 20‑40%) to the provider; you retain the rest. |

| Repayment | Interest rolls up; final repayment on sale or after death. | Provider receives their share when the property is sold. |

| Interest | Charged daily; rates vary 4‑6% APR. | No interest, but discount on the portion sold (usually 20‑30%). |

| Impact on inheritance | Debt reduces estate value; heirs inherit after loan settlement. | Heirs inherit only the retained share; provider’s share is fixed. |

| Eligibility | Usually 55+; full health assessment may be required. | Often 60+; some providers impose health checks. |

How to Assess Your Suitability

Follow this step‑by‑step checklist to decide if equity release is right for you.

- Calculate your property value using recent sales data or a professional appraisal.

- Determine the outstanding balance on any existing mortgage. Subtract this from the total value to get net equity.

- Check your age and health status. If you are under 55, look into alternative options like personal loans.

- Project your cash‑flow needs for the next 5‑10 years: medical bills, home upgrades, travel, or debt consolidation.

- Run a “what‑if” scenario: use an online calculator or spreadsheet to model interest accrual on a lifetime mortgage versus the discount on a home reversion share.

- Consult a qualified financial advisor experienced in retirement and property finance.

- Review the effect on any government benefits (e.g., Centrelink Age Pension) using the Services Australia eligibility tool.

Common Pitfalls and How to Avoid Them

Even qualified candidates can run into trouble if they overlook the fine print.

- Underestimating interest growth: Lifetime mortgage balances can double in 10‑15 years if rates climb. Use a worst‑case interest rate when modelling.

- Ignoring inheritance expectations: Discuss plans with family early to prevent surprise claims on the estate.

- Choosing the cheapest provider without checking service quality: Look for providers with transparent fees, good customer reviews, and member of the National Association of Equity Release Professionals (NAERP).

- Not securing independent legal advice: A solicitor can flag hidden charges, early repayment penalties, or restrictive covenants.

- Assuming the cash is tax‑free forever: While the lump sum isn’t taxed, the interest is not deductible, and the eventual sale may trigger capital gains tax for non‑primary residences.

Case Study: Jane and Mark, 68‑Year‑Old Retirees

Jane and Mark own a $950,000 home in Sydney. Their mortgage is $150,000, leaving $800,000 net equity. They need $200,000 for home renovations and a medical fund.

After consulting their financial advisor, they opted for a lifetime mortgage of $250,000 at 5.2% APR, which allowed them to keep full ownership. A 10‑year projection showed the loan would grow to $415,000, still well below the home’s expected market value.

They avoided a home reversion, which would have required selling a 25% share for an approximate $225,000 discount, reducing the inheritance for their grandchildren.

Key takeaway: matching the product to cash‑flow timing and inheritance goals made the lifetime mortgage the better fit.

Next Steps for Interested Homeowners

Ready to explore equity release? Here’s what to do next.

- Gather recent property valuation documents and mortgage statements.

- List your short‑term and long‑term financial goals.

- Book a free, no‑obligation consultation with a certified financial advisor.

- Ask for a transparent quote from at least two reputable equity release providers.

- Review the offer with a solicitor, focusing on interest accrual, repayment triggers, and any early exit fees.

- Make an informed decision and sign the agreement only after fully understanding the impact on your estate.

Frequently Asked Questions

What is the minimum age for equity release in Australia?

Most providers require you to be at least 55 years old, but better rates often appear after 65.

Can I still rent out a room after taking a lifetime mortgage?

Yes. Since you retain full ownership, you can rent out part of the property, but the borrowed amount may affect your loan‑to‑value ratio.

Will equity release affect my Centrelink pension?

A lump‑sum payment can be counted as income or assets, potentially reducing Age Pension entitlements. Always run the numbers through Services Australia.

Do I need a health assessment for a lifetime mortgage?

Many lenders perform a basic health questionnaire to gauge life expectancy, which influences the maximum loan amount they’ll offer.

What happens to the loan if I move into aged care?

The loan usually becomes due on sale of the property. Some providers allow the debt to be transferred to an aged‑care facility, but fees may apply.

Equity release can be a powerful tool when used by the right people. By checking age, property value, existing debt, and future inheritance goals, you can decide whether a lifetime mortgage or home reversion best supports your retirement lifestyle.