CD Interest Calculator

Calculate how much your $10,000 CD would earn in a year at current rates. Based on data from top banks as of late 2025.

If you’ve got $10,000 sitting in a certificate of deposit (CD), you’re probably wondering: how much will that actually earn me in a year? It’s not just about leaving money alone-it’s about making it work for you without risk. And right now, in late 2025, the answer isn’t what it was five years ago. Back then, you’d barely scrape together $50 a year. Today? You could be earning over $500-depending on where you put it.

What’s a CD, Really?

A certificate of deposit isn’t a stock, crypto, or mutual fund. It’s a bank product that pays you interest in exchange for locking your money away for a set time-three months, one year, five years. The bank uses your cash to lend to others, and they share a portion of that profit with you. It’s safe. FDIC-insured up to $250,000 per account. No market swings. No surprises. Just steady, predictable returns.

But not all CDs are the same. Rates change constantly. A CD you opened in January 2025 might pay 4.25%, while one opened in November pays 4.85%. That’s a $60 difference on $10,000. And if you’re shopping around, you’ll find online banks offering better deals than your local branch.

How Much Does a $10,000 CD Earn in 2025?

Let’s break it down with real numbers from today’s market. Based on data from FDIC and top online banks as of December 2025, here’s what you can expect:

- 1-year CD at 4.75%: $475 in interest

- 1-year CD at 4.25%: $425 in interest

- 5-year CD at 4.50%: $450 per year (but locked in for five years)

- High-yield savings account (for comparison): $4.00% = $400/year

That means a $10,000 CD at the average 1-year rate right now earns you about $475. That’s nearly 5% return-more than most savings accounts, and without the volatility of stocks.

And here’s the kicker: interest compounds. If your CD pays monthly (most do), you’re not just earning 4.75% on $10,000. You’re earning it on $10,000 plus the interest you’ve already earned. After a full year, that adds about $2-$3 extra. Not life-changing, but every dollar counts.

Where to Find the Best CD Rates

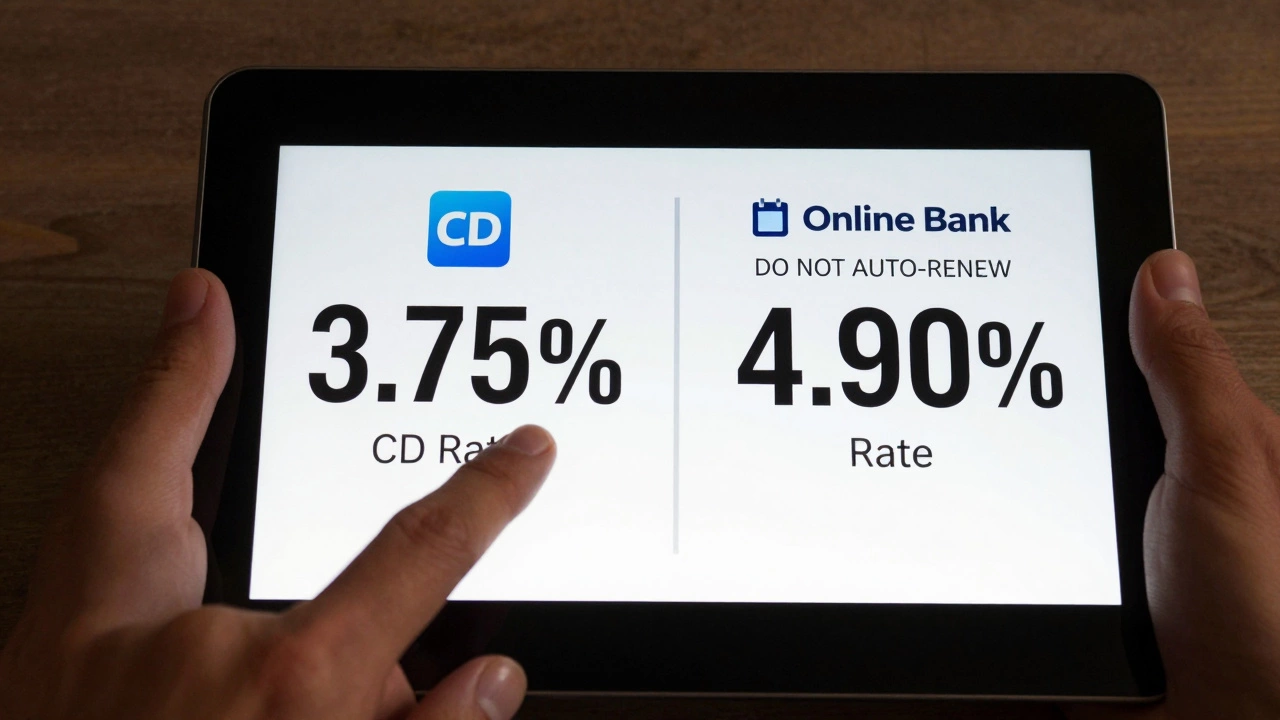

Your local bank? Probably not. Branch banks like Chase or Bank of America are still offering 1-year CDs around 3.75%-if they’re offering any at all. The real money is online.

Online banks like Ally, Marcus by Goldman Sachs, and Synchrony have been leading the pack in 2025. Why? Lower overhead. No branches to maintain. They pass the savings to you.

For example:

- Ally Bank: 4.85% APY on 1-year CD (minimum $2,000)

- Marcus: 4.70% APY (no minimum, no fees)

- Synchrony: 4.90% APY (requires $2,000, 12-month term)

That’s a $150 difference between the lowest and highest rate on a $10,000 CD. You don’t need to be a financial expert to spot that gap. Just spend 20 minutes comparing rates on Bankrate or NerdWallet.

What About Early Withdrawal Penalties?

CDs aren’t like checking accounts. You can’t pull your money out anytime you want. If you do, you’ll pay a penalty. Most banks charge 90 days’ worth of interest for a 1-year CD. So if you earn $475 and cash out after six months, you might lose $118. That leaves you with $357.

That’s why you need to be sure you won’t need the cash. Think of it like a vacation fund or a car down payment you won’t touch for a year. If you’re unsure, go with a high-yield savings account instead. You’ll earn less-maybe $400-but you keep full access.

CD Laddering: Make More Without Risk

What if you have $30,000 to invest? Or you want to keep some flexibility? That’s where CD laddering comes in.

Instead of putting all $10,000 into a 1-year CD, split it:

- Put $3,333 into a 1-year CD

- Put $3,333 into a 2-year CD

- Put $3,334 into a 3-year CD

After one year, your first CD matures. You take that $3,333 and roll it into a new 3-year CD. Now you’ve got one CD maturing every year, always earning the highest available rate. And you never have all your money locked up.

It’s a simple trick. But it’s used by people who’ve built $500,000 in CDs over time. They don’t chase the highest rate every month-they build a system.

CDs vs. Savings Accounts: What’s Better?

Let’s compare apples to apples:

| Feature | 1-Year CD | High-Yield Savings Account |

|---|---|---|

| APY | 4.75% | 4.00% |

| Yearly Earnings | $475 | $400 |

| Access to Funds | Locked for 12 months | Instant |

| Penalty for Early Withdrawal | 90 days’ interest | None |

| FDIC Insured | Yes | Yes |

If you’re saving for a known expense in 12 months-like a wedding, a new appliance, or a tax bill-the CD wins. If you’re building an emergency fund? Go with the savings account. You don’t want to be stuck without cash when your car breaks down.

Is a CD Worth It in 2025?

Yes-if you know what you’re getting into. CDs aren’t flashy. They don’t make headlines. But they’re one of the few places where you can lock in a guaranteed return that beats inflation.

In 2025, inflation is hovering around 2.8%. A 4.75% CD gives you a real return of nearly 2%. That’s not just keeping up-it’s growing. And it’s safer than keeping cash under a mattress.

And if you’re retired or risk-averse? CDs are the quiet backbone of your portfolio. They don’t promise excitement. They promise reliability.

What to Watch Out For

Not all CDs are created equal. Here are three traps to avoid:

- Bonus rates: Some banks offer a higher rate for the first year, then drop it. Read the fine print. The advertised rate isn’t always the long-term rate.

- Minimum deposits: Some CDs require $5,000 or $10,000. If you’re under that, you won’t qualify. Check before you apply.

- Automatic renewal: Many CDs roll over automatically when they mature. If you forget, you could get stuck at a lower rate. Set a calendar reminder.

Always read the terms. A 10-minute review can save you hundreds.

Final Answer: How Much Does a $10,000 CD Make in a Year?

As of December 2025, a $10,000 CD earns between $425 and $490 in interest over 12 months, depending on the bank and rate. The average is around $475. That’s $39.50 per month. Enough to cover a few groceries, a tank of gas, or a weekend getaway.

It’s not going to make you rich. But in a world where savings accounts pay less than 1% and stocks are unpredictable, it’s one of the smartest, simplest moves you can make with cash you don’t need right now.